Source: Unemployment/unemployment.Rmd

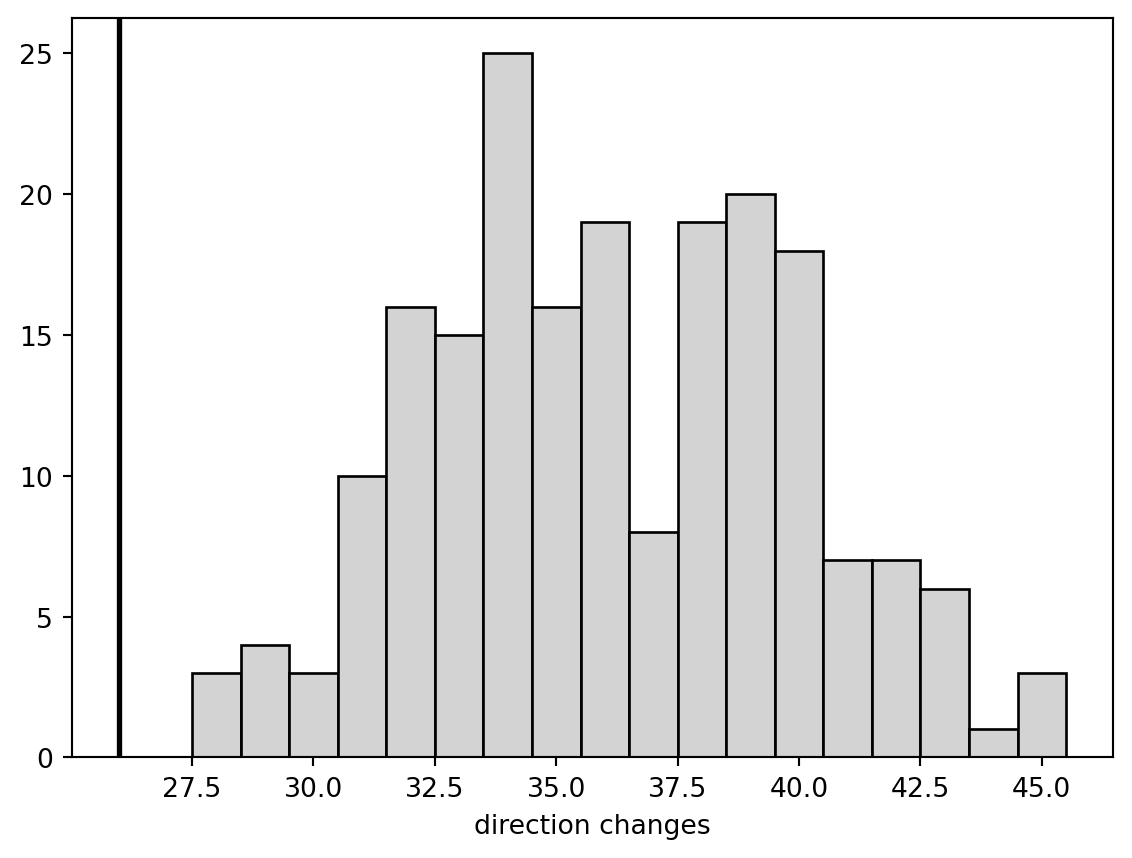

The original fits a first-order autoregression and checks whether simulated unemployment series reproduce the observed sign-change behavior.

Code

from pathlib import Pathimport numpy as npimport pandas as pdimport matplotlib.pyplot as pltimport statsmodels.formula.api as smf= Path("../../ROS-Examples" )= pd.read_table(root / "Unemployment/data/unemp.txt" , sep= r" \s + " )

0

1947

3.9

1

1948

3.8

2

1949

5.9

3

1950

5.3

4

1951

3.3

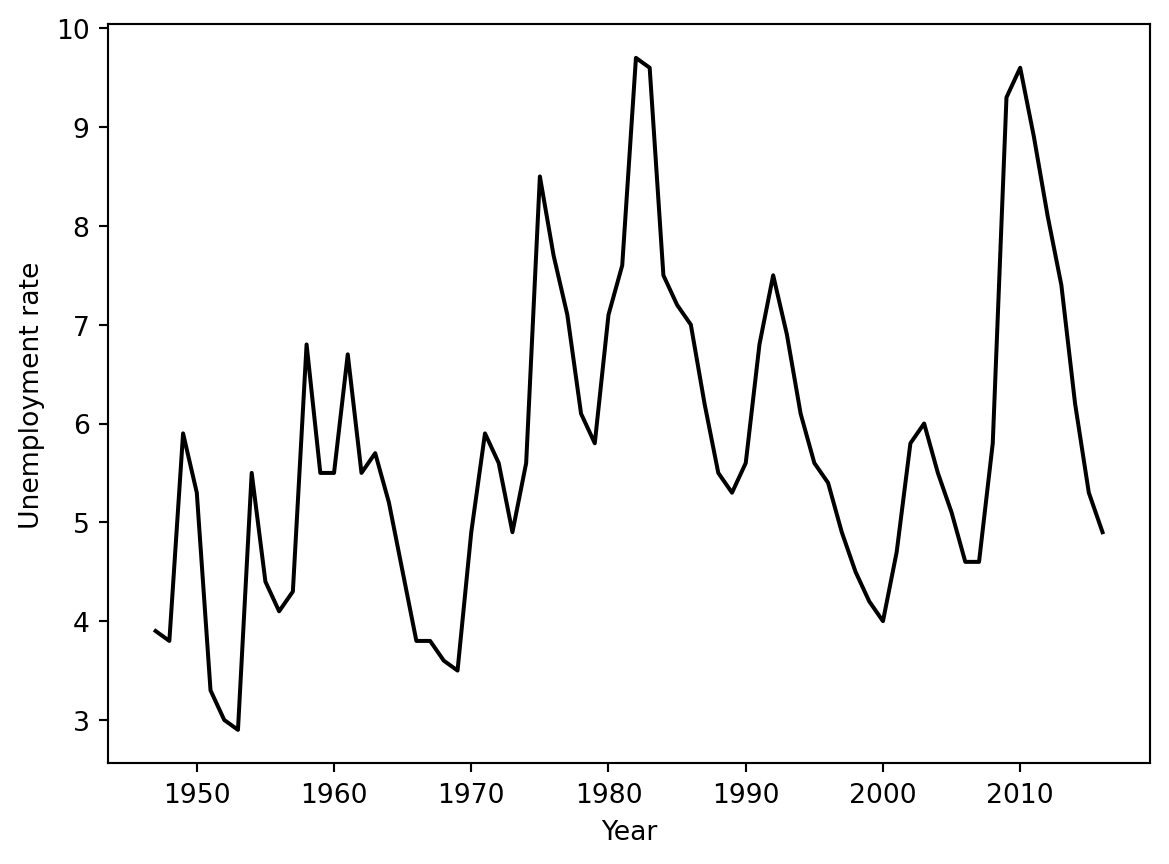

Plot the series

Code

= plt.subplots()= "black" )"Year" )"Unemployment rate" )

Text(0, 0.5, 'Unemployment rate')

AR(1) fit

Code

"y_lag" ] = unemp.y.shift(1 )= smf.ols("y ~ y_lag" , data= unemp.dropna()).fit()

OLS Regression Results

Dep. Variable:

y

R-squared:

0.601

Model:

OLS

Adj. R-squared:

0.595

Method:

Least Squares

F-statistic:

100.7

Date:

Sun, 31 May 2026

Prob (F-statistic):

5.54e-15

Time:

23:05:54

Log-Likelihood:

-98.513

No. Observations:

69

AIC:

201.0

Df Residuals:

67

BIC:

205.5

Df Model:

1

Covariance Type:

nonrobust

coef

std err

t

P>|t|

[0.025

0.975]

Intercept

1.3536

0.461

2.939

0.005

0.434

2.273

y_lag

0.7688

0.077

10.036

0.000

0.616

0.922

Omnibus:

20.288

Durbin-Watson:

1.582

Prob(Omnibus):

0.000

Jarque-Bera (JB):

26.717

Skew:

1.254

Prob(JB):

1.58e-06

Kurtosis:

4.733

Cond. No.

23.0

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

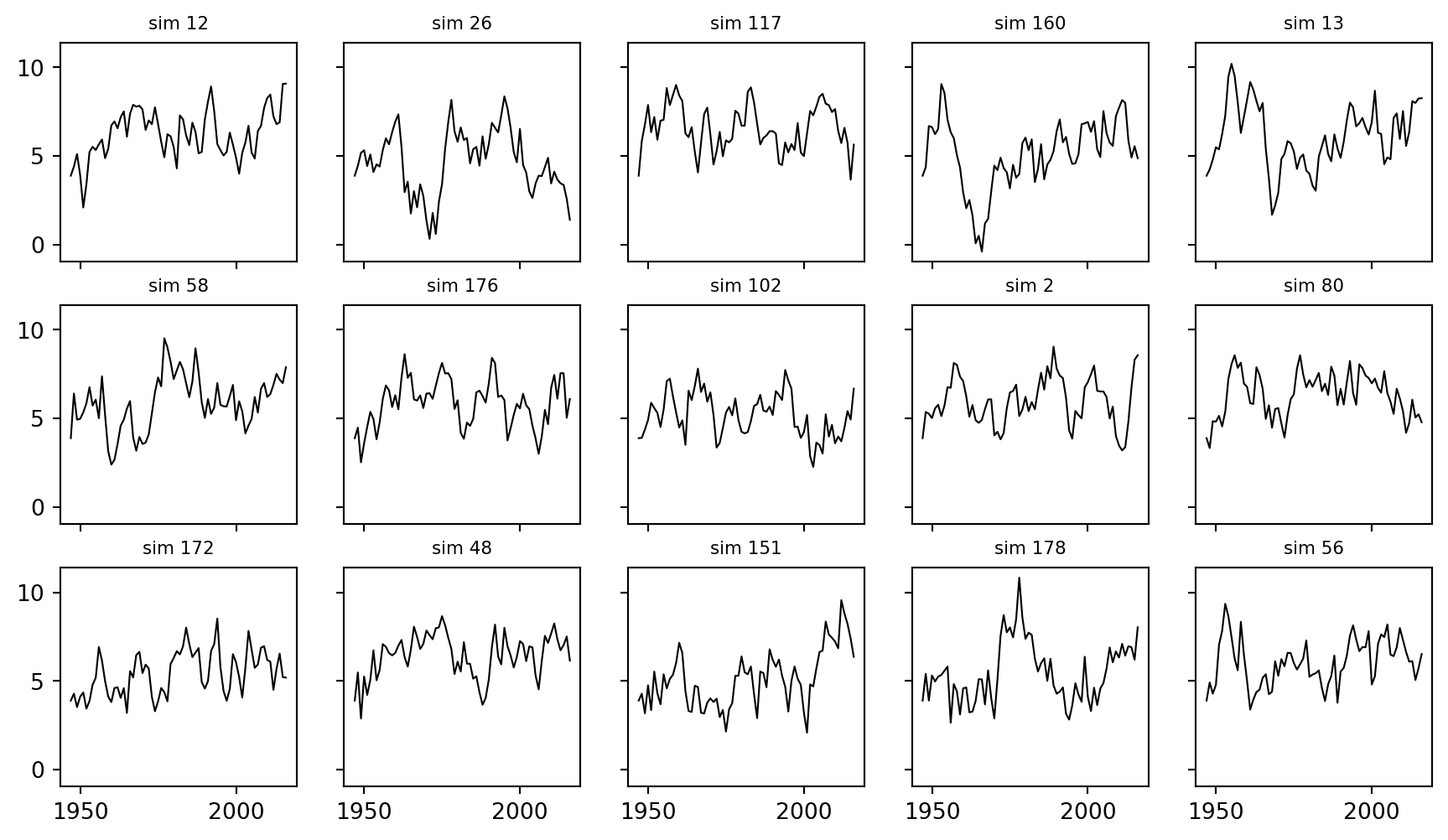

Simulate replicated series

Code

= np.random.default_rng(123 )= len (unemp)= 200 = np.sqrt(fit_lag.mse_resid)= fit_lag.params["Intercept" ], fit_lag.params["y_lag" ]= np.empty((S, n))0 ] = unemp.y.iloc[0 ]for s in range (S):for t in range (1 , n):= a + b * y_rep[s, t- 1 ] + rng.normal(0 , sigma)

Code

= plt.subplots(3 , 5 , figsize= (11 , 6 ), sharex= True , sharey= True )for ax, s in zip (axs.ravel(), rng.choice(S, 15 , replace= False )):= "black" , linewidth= 0.8 )f"sim { s} " , fontsize= 8 )

Test statistic: changes in direction

Code

def direction_changes(y):= np.asarray(y)return np.sum (np.sign(y[2 :] - y[1 :- 1 ]) != np.sign(y[1 :- 1 ] - y[:- 2 ]))= direction_changes(unemp.y)= np.apply_along_axis(direction_changes, 1 , y_rep)print (test_y, np.mean(test_rep > test_y), np.quantile(test_rep, [0.1 , 0.5 , 0.9 ]))

Code

= plt.subplots()= np.arange(test_rep.min (), test_rep.max ()+ 2 )- 0.5 , color= "lightgray" , edgecolor= "black" )= "black" , linewidth= 2 )"direction changes" )

Text(0.5, 0, 'direction changes')