# National Election Study: logistic regression, prediction, and separation

Source: `NES/nes_logistic.Rmd`

This page ports the ROS logistic-regression example. It uses the 1992 National Election Study for a simple vote-on-income model, then repeats logistic regressions across years to show changing income effects and the instability created by separation.

## Setup and data

```{python}

from pathlib import Path

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

import statsmodels.formula.api as smf

from scipy.special import expit

from python.bayes_glm import bayes_logit

root = Path("../../ROS-Examples")

nes_dir = root / "NES"

nes = pd.read_csv(nes_dir / "data/nes.txt", sep=r"\s+", index_col=0, na_values=["NA"])

nes.head()

```

The source R page first keeps 1992 respondents with a valid Democratic or Republican presidential vote.

```{python}

ok92 = (nes["year"] == 1992) & nes["rvote"].notna() & nes["dvote"].notna() & ((nes["rvote"] == 1) | (nes["dvote"] == 1))

nes92 = nes.loc[ok92].copy()

nes92[["year", "income", "rvote", "dvote", "presvote"]].head()

```

## A single-predictor logistic regression

The R model is `stan_glm(rvote ~ income, family=binomial(link="logit"))`. For the main Bayesian port, fit the same Bernoulli-logit model with weak Normal priors using the shared lightweight helper.

```{python}

fit_1 = bayes_logit("rvote ~ income", data=nes92, draws=4000, prior_scale=2.5, seed=1992)

fit_1.summary()

```

```{python}

new = pd.DataFrame({"income": [5]})

eta_draw = fit_1.beta_draws @ np.array([1.0, 5.0])

p_draw = expit(eta_draw)

pd.DataFrame({

"linear_predictor_mean": [eta_draw.mean()],

"linear_predictor_sd": [eta_draw.std(ddof=1)],

"expected_probability_mean": [p_draw.mean()],

"expected_probability_sd": [p_draw.std(ddof=1)],

})

```

The distinction among linear predictor, expected outcome, and posterior predictive draw is clearest when using the posterior coefficient draws directly. This mirrors the operations performed by `posterior_linpred`, `posterior_epred`, and `posterior_predict` in the R example.

```{python}

rng = np.random.default_rng(1992)

draws = fit_1.beta_draws

X_new = np.column_stack([np.ones(5), np.arange(1, 6)])

linpred = draws @ X_new.T

epred = expit(linpred)

postpred = rng.binomial(1, epred)

summary_pred = pd.DataFrame(

{

"income": np.arange(1, 6),

"p_mean": epred.mean(axis=0),

"p_sd": epred.std(axis=0),

"y_pred_mean": postpred.mean(axis=0),

}

)

summary_pred

```

```{python}

prob_rich_gt_next = np.mean(epred[:, 4] > epred[:, 3])

diff_interval = np.quantile(epred[:, 4] - epred[:, 3], [0.025, 0.975])

prob_rich_gt_next, diff_interval

```

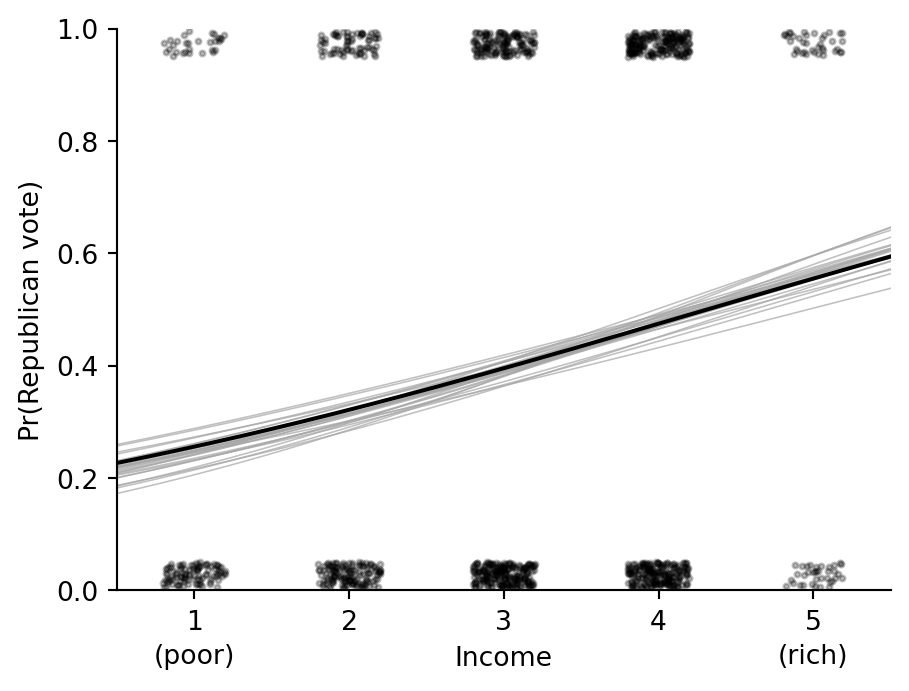

## Jittered data and fitted curve

```{python}

rng = np.random.default_rng(2141)

n = len(nes92)

income_jitt = nes92["income"].to_numpy() + rng.uniform(-0.2, 0.2, size=n)

vote_jitt = nes92["rvote"].to_numpy() + np.where(nes92["rvote"].to_numpy() == 0, rng.uniform(0.005, 0.05, size=n), rng.uniform(-0.05, -0.005, size=n))

x_grid = np.linspace(0.5, 5.5, 200)

X_grid = pd.DataFrame({"income": x_grid})

fig, ax = plt.subplots(figsize=(5.2, 3.8))

for draw in draws[rng.choice(len(draws), 25, replace=False)]:

ax.plot(x_grid, expit(draw[0] + draw[1] * x_grid), color="0.65", lw=0.6, alpha=0.7)

ax.plot(x_grid, fit_1.epred(X_grid).mean(axis=0), color="black", lw=1.5)

ax.scatter(income_jitt, vote_jitt, s=4, color="black", alpha=0.25)

ax.set_xticks(range(1, 6))

ax.text(1, -0.13, "(poor)", ha="center", transform=ax.get_xaxis_transform())

ax.text(5, -0.13, "(rich)", ha="center", transform=ax.get_xaxis_transform())

ax.set(xlim=(0.5, 5.5), ylim=(0, 1), xlabel="Income", ylabel="Pr(Republican vote)")

ax.spines[["top", "right"]].set_visible(False)

```

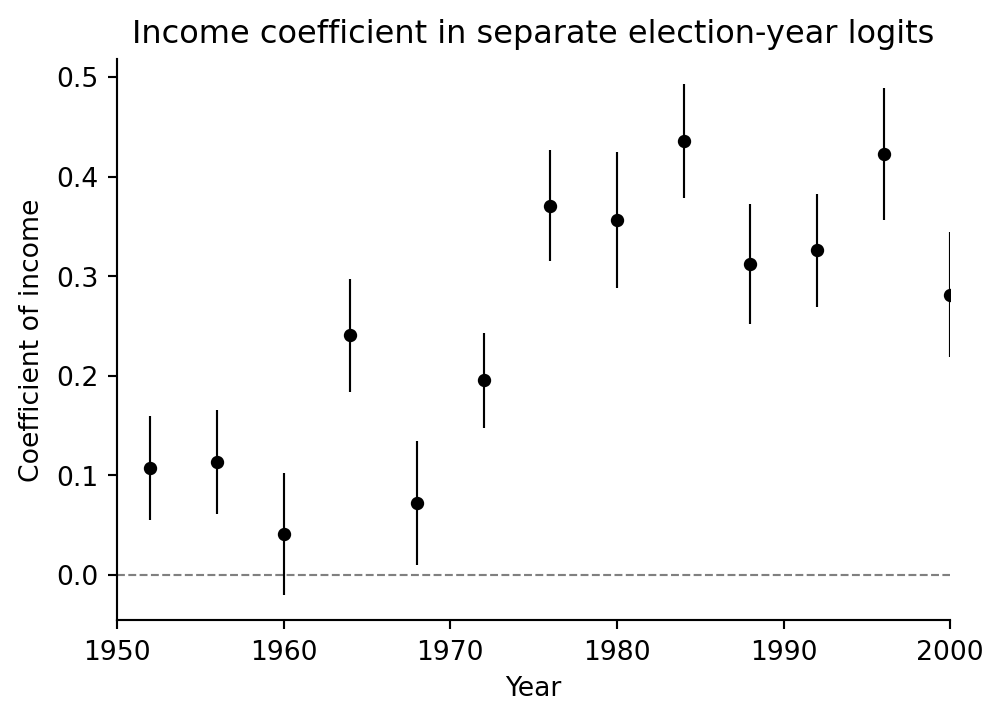

## Income coefficient by election year

```{python}

years = list(range(1952, 2001, 4))

rows = []

for year in years:

ok = (nes["year"] == year) & nes["presvote"].notna() & (nes["presvote"] < 3) & nes["vote"].notna() & nes["income"].notna()

d = nes.loc[ok, ["presvote", "income"]].copy()

d["vote_rep"] = d["presvote"] - 1

if d["vote_rep"].nunique() < 2:

continue

fit_y = smf.glm("vote_rep ~ income", data=d, family=sm.families.Binomial()).fit()

rows.append({"year": year, "coef": fit_y.params["income"], "se": fit_y.bse["income"], "nobs": fit_y.nobs})

fits = pd.DataFrame(rows)

fits

```

```{python}

fig, ax = plt.subplots(figsize=(5.6, 3.8))

ax.axhline(0, color="0.5", ls="--", lw=0.8)

ax.errorbar(fits["year"], fits["coef"], yerr=fits["se"], fmt="o", color="black", ms=4, lw=0.8)

ax.set(xlim=(1950, 2000), xlabel="Year", ylabel="Coefficient of income", title="Income coefficient in separate election-year logits")

ax.spines[["top", "right"]].set_visible(False)

```

## In-sample accuracy and log score

```{python}

predp = fit_1.epred().mean(axis=0)

y = nes92["rvote"].to_numpy()

accuracy_parts = (predp[y == 1].mean(), (1 - predp[y == 0]).mean())

log_score = np.log(np.r_[predp[y == 1], 1 - predp[y == 0]]).sum()

accuracy_parts, log_score

```

A light leave-one-out calculation can be done by refitting the model after dropping each observation. This is slower than PSIS-LOO from the Stan ecosystem, but it is transparent for a simple GLM.

```{python}

def loo_log_score(data):

values = []

for i in data.index:

train = data.drop(index=i)

test = data.loc[[i]]

fit_i = smf.glm("rvote ~ income", data=train, family=sm.families.Binomial()).fit(disp=0)

p_i = fit_i.predict(test)[0]

y_i = test["rvote"].iloc[0]

values.append(np.log(p_i if y_i == 1 else 1 - p_i))

return np.sum(values)

# loo_log_score(nes92) # uncomment to run the exact leave-one-out refit

```

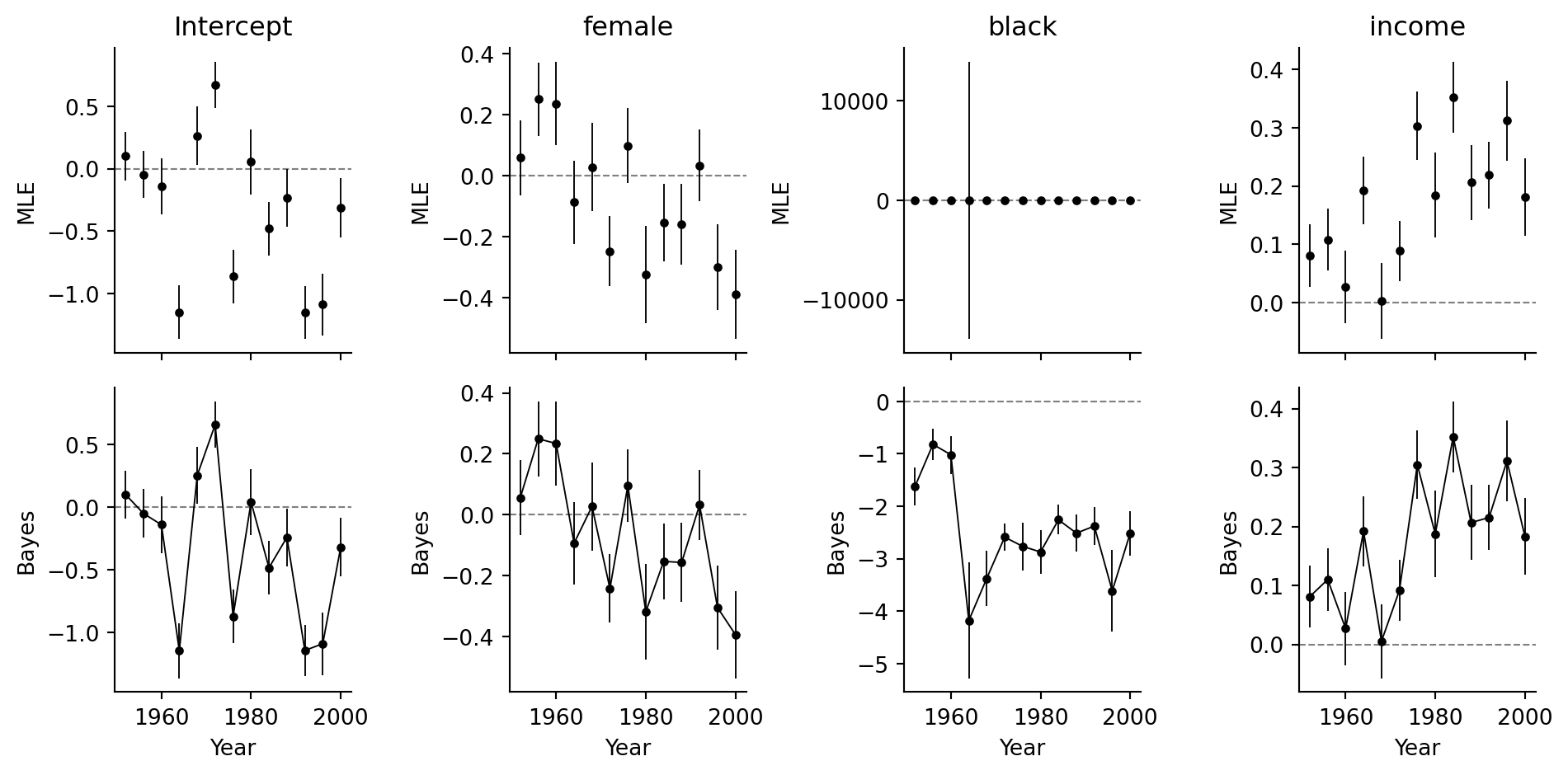

## Separation and weak regularization

The final part of the source example compares classical `glm` with `stan_glm` for `rvote ~ female + black + income`. In years with quasi-complete separation, maximum-likelihood coefficients can become huge or have enormous standard errors. A weakly regularized logistic model stabilizes the fit.

```{python}

terms = ["Intercept", "female", "black", "income"]

sep_rows = []

base = nes.loc[nes[["rvote", "female", "black", "income"]].notna().all(axis=1)].copy()

for year in years:

d = base.loc[base["year"] == year].copy()

if d["rvote"].nunique() < 2:

continue

try:

fit_glm = smf.glm("rvote ~ female + black + income", data=d, family=sm.families.Binomial()).fit()

for term in terms:

sep_rows.append({"year": year, "term": term, "model": "MLE", "coef": fit_glm.params[term], "se": fit_glm.bse[term]})

except Exception as err:

sep_rows.append({"year": year, "term": "model", "model": "MLE", "coef": np.nan, "se": np.nan, "note": str(err)})

sep = pd.DataFrame(sep_rows)

sep.head()

```

The Bayesian fit uses the same weak Normal prior in every year. Its posterior mean and standard deviation stay finite when the likelihood alone is weakly identified.

```{python}

reg_rows = []

for year in years:

d = base.loc[base["year"] == year].copy()

if d["rvote"].nunique() < 2:

continue

fit_bayes_y = bayes_logit("rvote ~ female + black + income", data=d, draws=2000, prior_scale=2.5, seed=year)

for term, coef, se in zip(fit_bayes_y.coef_names, fit_bayes_y.beta_draws.mean(axis=0), fit_bayes_y.beta_draws.std(axis=0, ddof=1)):

reg_rows.append({"year": year, "term": term, "model": "Bayes normal-prior", "coef": coef, "se": se})

regularized = pd.DataFrame(reg_rows)

regularized.head()

```

```{python}

fig, axes = plt.subplots(2, 4, figsize=(10, 5), sharex=True)

for col, term in enumerate(terms):

d_mle = sep.loc[sep["term"] == term]

axes[0, col].axhline(0, color="0.5", ls="--", lw=0.8)

axes[0, col].errorbar(d_mle["year"], d_mle["coef"], yerr=d_mle["se"], fmt="o", color="black", ms=3, lw=0.7)

axes[0, col].set_title(term)

axes[0, col].set_ylabel("MLE")

d_reg = regularized.loc[regularized["term"] == term]

axes[1, col].axhline(0, color="0.5", ls="--", lw=0.8)

axes[1, col].errorbar(d_reg["year"], d_reg["coef"], yerr=d_reg["se"], fmt="o-", color="black", ms=3, lw=0.7)

axes[1, col].set_ylabel("Bayes")

axes[1, col].set_xlabel("Year")

for ax in axes.ravel():

ax.set_xticks([1960, 1980, 2000])

ax.spines[["top", "right"]].set_visible(False)

fig.tight_layout()

```

## CmdStanPy version of the single-predictor model

Use this small Stan model if exact Stan sampling is needed instead of the lightweight Laplace posterior used above.

```{python}

from cmdstanpy import CmdStanModel

stan_code = """

data {

int<lower=1> N;

vector[N] income;

array[N] int<lower=0, upper=1> rvote;

}

parameters {

real alpha;

real beta;

}

model {

alpha ~ normal(0, 2.5);

beta ~ normal(0, 2.5);

rvote ~ bernoulli_logit(alpha + beta * income);

}

"""

stan_file = Path("_generated/nes_vote_income.stan")

stan_file.parent.mkdir(exist_ok=True)

stan_file.write_text(stan_code)

model = CmdStanModel(stan_file=str(stan_file))

fit = model.sample(

data={"N": len(nes92), "income": nes92["income"].to_numpy(), "rvote": nes92["rvote"].astype(int).to_list()},

seed=1992,

chains=4,

parallel_chains=4,

show_progress=False,

)

fit.draws_pd()[["alpha", "beta"]].describe(percentiles=[0.05, 0.5, 0.95])

```