from pathlib import Pathimport pandas as pdBASE = Path('/Users/alal/tmp/cate_policy')ASSETS = BASE /'report_assets'summary = pd.read_csv(ASSETS /'summary.csv')summary_rounded = summary.copy()for col in summary_rounded.columns[1:]: summary_rounded[col] = summary_rounded[col].map(lambda x: round(float(x), 4))summary_rounded

method

profit_mean

profit_sd

regret_mean

regret_sd

mse_mean

mse_sd

0

Oracle

0.4451

0.0024

0.0000

0.0000

0.0000

0.0000

1

policyCATE logistic σ=0.25

0.4432

0.0041

0.0018

0.0034

2.6670

2.2311

2

policyCATE logistic σ=0.75

0.4126

0.0153

0.0325

0.0152

0.5249

0.0797

3

policyCATE logistic σ=2.0

0.3833

0.0175

0.0617

0.0175

0.4639

0.0142

4

policyCATE uniform (OLS special case)

0.3771

0.0177

0.0680

0.0176

0.4615

0.0103

5

LinearDML

0.3763

0.0047

0.0688

0.0042

0.4505

0.0029

What this is

I pulled the TeX source for arXiv:2512.13400 and implemented the paper’s linear M-estimator in trex.policy_learning.policyCATElearner.

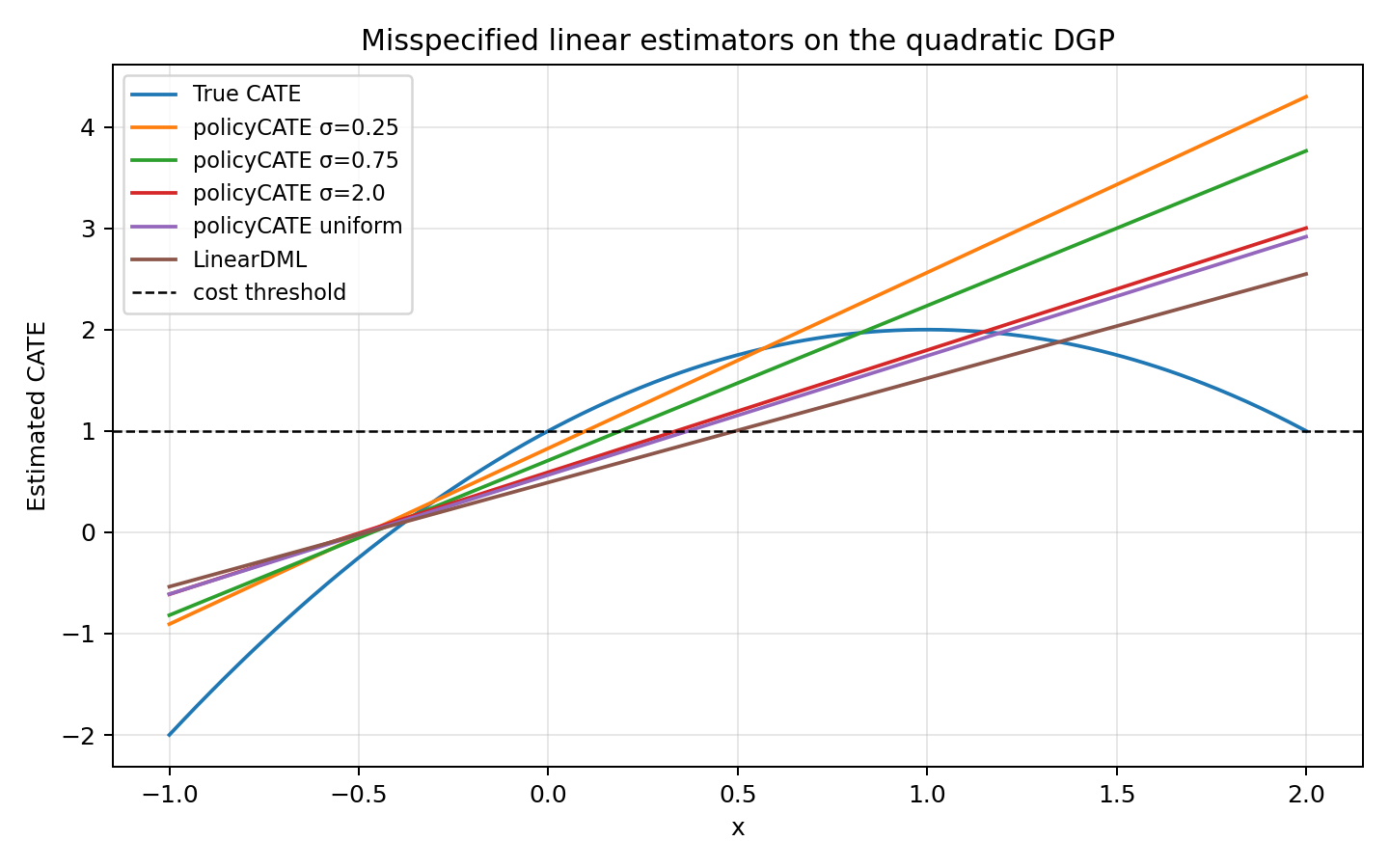

The comparison below uses the paper’s simple quadratic DGP, but with a deliberately misspecified linear CATE model. That is the case where the paper argues decision-focused fitting should help most.

treatment cost: c = 1

train size per replication: 4000

test size per replication: 30000

replications: 25

regret: oracle profit minus realized policy profit

Methods compared

Oracle assignment

econml.dml.LinearDML

policyCATElearner with logistic surrogate at three σ values

policyCATElearner with the uniform surrogate, which collapses to transformed-outcome OLS

Summary table

Show code

summary_rounded

method

profit_mean

profit_sd

regret_mean

regret_sd

mse_mean

mse_sd

0

Oracle

0.4451

0.0024

0.0000

0.0000

0.0000

0.0000

1

policyCATE logistic σ=0.25

0.4432

0.0041

0.0018

0.0034

2.6670

2.2311

2

policyCATE logistic σ=0.75

0.4126

0.0153

0.0325

0.0152

0.5249

0.0797

3

policyCATE logistic σ=2.0

0.3833

0.0175

0.0617

0.0175

0.4639

0.0142

4

policyCATE uniform (OLS special case)

0.3771

0.0177

0.0680

0.0176

0.4615

0.0103

5

LinearDML

0.3763

0.0047

0.0688

0.0042

0.4505

0.0029

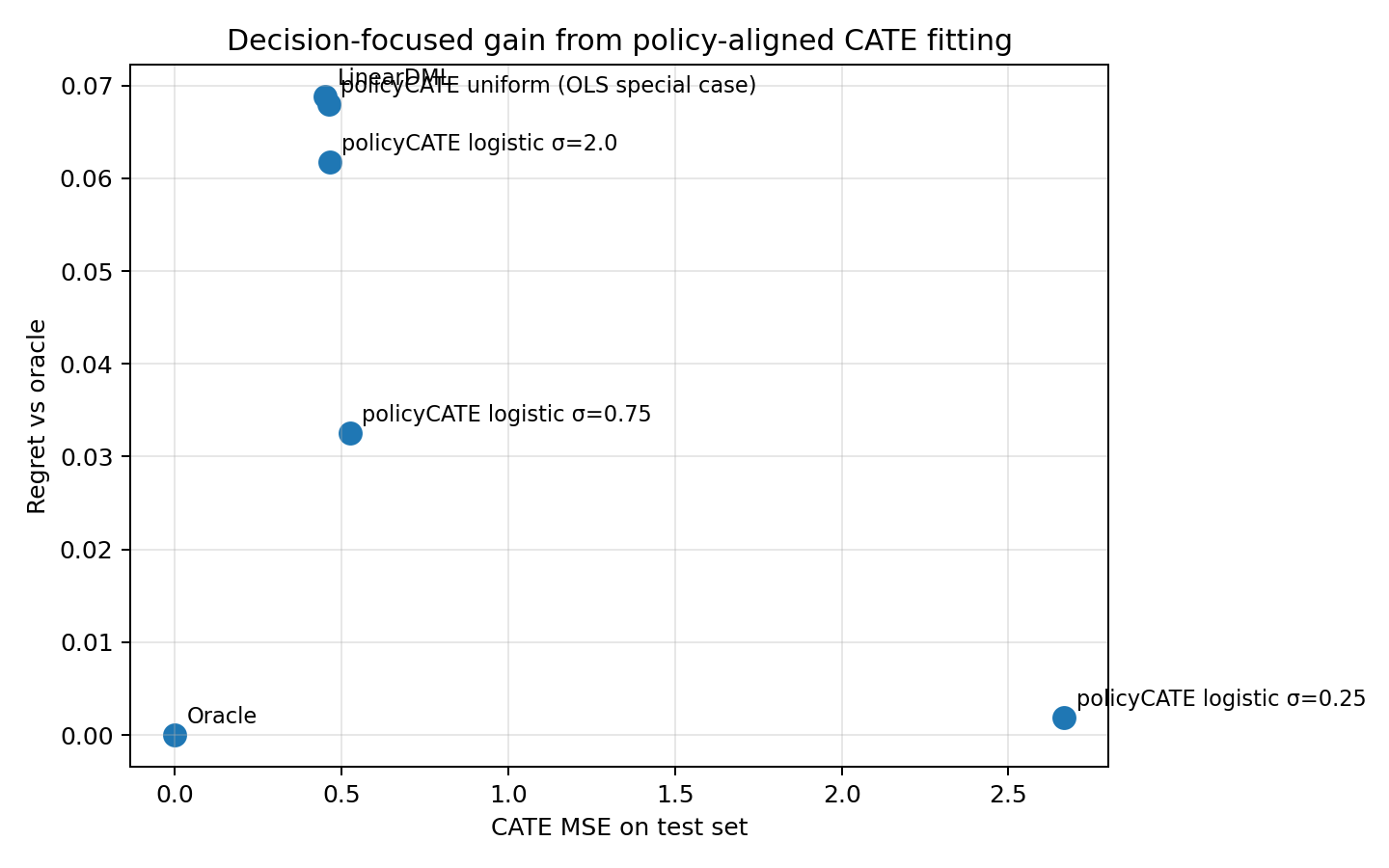

Profit-regret tradeoff

Fitted CATE curves on one draw

Paper distillation

Here is the implementation-level distillation of the paper.

Core idea

The paper starts from the firm’s targeting rule: treat when the true CATE exceeds the treatment cost \(c\).

Instead of optimizing a hard threshold at \(c\), it randomizes the threshold as \(C \sim F_C(c, \sigma)\) and maximizes the resulting smooth surrogate. At the population level, for a scalar candidate effect \(\tau\), the objective is

This is basically weighted residual fitting, but the weights are endogenous and largest near the decision boundary. That is the paper’s “Decision Attention” mechanism.

large \(\sigma\): broad weighting, close to ordinary transformed-outcome MSE

small \(\sigma\): concentrated weighting near \(\tau \approx c\), closer to direct policy optimization

which recovers transformed-outcome OLS as a special case.

Why this is useful

The framework continuously interpolates between three familiar objects:

plug-in CATE estimation via squared error

direct policy optimization as \(\sigma \to 0\)

entropy-regularized sigmoid policy learning under the logistic choice

So it is not just a new loss. It is a clean bridge between prediction-focused CATE estimation and profit-focused policy learning.

Practical implementation takeaways

For implementation, the paper strongly suggests:

start with the logistic surrogate

use regularization, especially when \(\sigma\) is small

warm start along a continuation path from large \(\sigma\) to small \(\sigma\)

tune \(\sigma\) on held-out policy value if profit is the real target

That is exactly why the small-\(\sigma\) model in the comparison above can have much worse global CATE MSE but much lower regret.

Read

A few things stand out.

Small \(\sigma\) sharply reduces regret, even though it makes global CATE MSE much worse.

The uniform special case behaves like plain transformed-outcome OLS.

LinearDML is competitive on MSE, but on this misspecified decision problem it still leaves materially more profit on the table than the tighter policy-focused surrogate.

This is exactly the paper’s point: if the business objective is treatment assignment, uniform accuracy is not the right target.