Minimum-Distance Estimation on a Cohort-by-Event-Time Lattice

Author

Apoorva Lal

Published

July 16, 2026

Abstract

Staggered-adoption event studies present an unresolved bias-variance tradeoff. A pooled event-study regression is precise and can fail to estimate an interpretable average treatment-effect curve when effects differ across adoption cohorts. A saturated cohort-by-event-time estimator accommodates that heterogeneity and can be noisy when there are many small cohorts. This paper proposes an adaptive estimator between those endpoints. Starting from a saturated heterogeneity-robust estimate, we construct minimum-distance projections onto a nested lattice of adjacent cohort and event-time partitions. Every candidate estimates the same support-aware aggregate event-study curve. A Lepskii rule selects the lowest-dimensional candidate whose curve agrees statistically with every finer comparable model. Cross-model covariance and a simultaneous critical value are obtained from the saturated regression’s cluster influence functions. Hyperparameter grids are tuned by honest nested cluster splitting against an independent saturated target estimate. Simulations with nine uneven adoption cohorts show that the selector recovers cohort-only, time-only, and tensor-product structure while approaching saturation when pooling distorts the target. The method is implemented as a pyfixest-compatible Python class.

1. Introduction

The recent difference-in-differences literature has clarified why a conventional two-way fixed-effects (TWFE) event study can fail to estimate a meaningful average of heterogeneous treatment effects under staggered adoption (Goodman-Bacon 2021; Chaisemartin and D’Haultfœuille 2020; Goldsmith-Pinkham, Hull, and Kolesár 2024). A direct response is to estimate treatment effects separately for every adoption cohort and event time, then aggregate the resulting cells using transparent nonnegative weights (Sun and Abraham 2021; Callaway and Sant’Anna 2021; Wooldridge 2021). That response protects the estimand and introduces a potentially large collection of noisy cohort-time coefficients.

This paper treats the choice between pooled and saturated event studies as an adaptive estimation problem. The motivating joint-test approach in Lal (2025) asks whether cohort-specific deviations from a common event-study curve are jointly zero. The test supplies a useful binary diagnostic. Rejection leaves the appropriate degree of partial pooling unresolved, and nonrejection leaves the magnitude of pooling bias unresolved. The resulting estimation problem is to determine how much structured heterogeneity the data can support.

The selection logic follows Lepskii’s comparison-to-refinement principle (Lepski 1990; Lepski and Spokoiny 1997; Goldenshluger and Lepski 2011). It is also related to recent work on adaptation to misspecification, where efficiency gains from a restricted model are weighed against detectable departures from that model (Armstrong, Kline, and Sun 2025). Our setting differs because the candidate class is a two-dimensional partial order and every model must be mapped to the same dynamic treatment-effect target.

We propose a two-axis partial-pooling estimator. The first axis groups adjacent adoption cohorts. The second groups adjacent event times, while preserving the pre/post boundary. Crossing the two partitions produces rectangular restrictions on the cohort-by-event-time treatment-effect surface. The coarsest candidates have a few interpretable blocks; the finest candidate is saturated. All candidates are linear minimum-distance projections of one saturated estimate, and all are mapped to the same support-aware aggregate event-study target.

The estimator has three useful features. First, one expensive fixed-effects regression produces the entire candidate path. Second, because every candidate is a linear transformation of the same saturated estimator, cross-model covariance is available exactly from a shared influence-function stack. Third, a cluster multiplier bootstrap can calibrate one critical value simultaneously over candidate models, refinements, and event times.

The paper makes four contributions.

It formulates partial pooling over a nested cohort-time lattice while holding the reported event-study estimand fixed.

It derives the minimum-distance candidate estimators and their joint covariance from a saturated heterogeneity-robust fit.

It gives a Lepskii selection rule and an honest nested-splitting procedure for tuning the candidate grid without using final-sample performance.

It implements the procedure in Python and evaluates risk, oracle regret, coverage, selection, and computation in a repeated many-cohort experiment.

The selected complexity pertains to a particular aggregate target. Distinct cohort effects may cancel under that target, making pooling useful for the aggregate curve while leaving the latent surface heterogeneous. Claims about full-surface homogeneity require a surface-level selection criterion. This distinction is central to interpreting the results.

2. Setup and Target

The introduction motivates a bias-variance tradeoff whose solution requires all candidate estimators to answer the same causal question. This section fixes that question, records which cohort-event cells are supported, and defines the saturated heterogeneity-robust estimator from which every later candidate is constructed. Its outputs are the base coefficient vector \hat\theta, covariance \hat\Sigma, influence contributions \hat\psi_c, and target map L used by the adaptive method in Section 3.

2.1 Staggered adoption

Units i=1,\ldots,n are observed in periods t=1,\ldots,T. Treatment adoption is absorbing:

D_{it}=1\{t\geq G_i\},

where G_i\in\mathcal G\cup\{\infty\} is the adoption date and G_i=\infty denotes a never-treated unit. Event time is s=t-G_i. Let \mathcal G_T=\{g_1<\cdots<g_J\} denote treated cohorts and let \mathcal S denote the reported event-time window, excluding the normalized reference period s=-1.

We maintain no anticipation, parallel trends for untreated potential outcomes, and overlap for every reported cell. The current implementation uses never-treated observations as the comparison group in a saturated interaction regression. The minimum-distance construction applies without change when the base vector and influence functions come from another identified heterogeneity-robust estimator.

2.2 Supported cells

Let \mathcal I\subseteq\mathcal G_T\times\mathcal S be the set of estimable cells. A cell enters \mathcal I only when it reaches a prespecified minimum support and the saturated design retains its coefficient. Unsupported cells receive zero target weight, and the remaining weights are renormalized over supported cohorts at each event time. This exposes the changing target population and prevents extrapolation of late event times for late adopters.

Stack supported effects in \theta\in\mathbb R^p. The reported dynamic ATT is

Post-treatment observations beyond the reporting window are trimmed, isolating the fixed effects from unmodeled tail effects. Earlier leads remain in the estimation sample under no anticipation. Let \hat\theta be the retained saturated coefficient vector and \hat\Sigma its cluster-robust covariance.

We assume the finite-dimensional asymptotic linear representation

where c indexes independent clusters. The scaling is absorbed into \hat\psi_c. In pyfixest, these contributions are constructed from the cluster sums of residualized regressor scores and the regression bread.

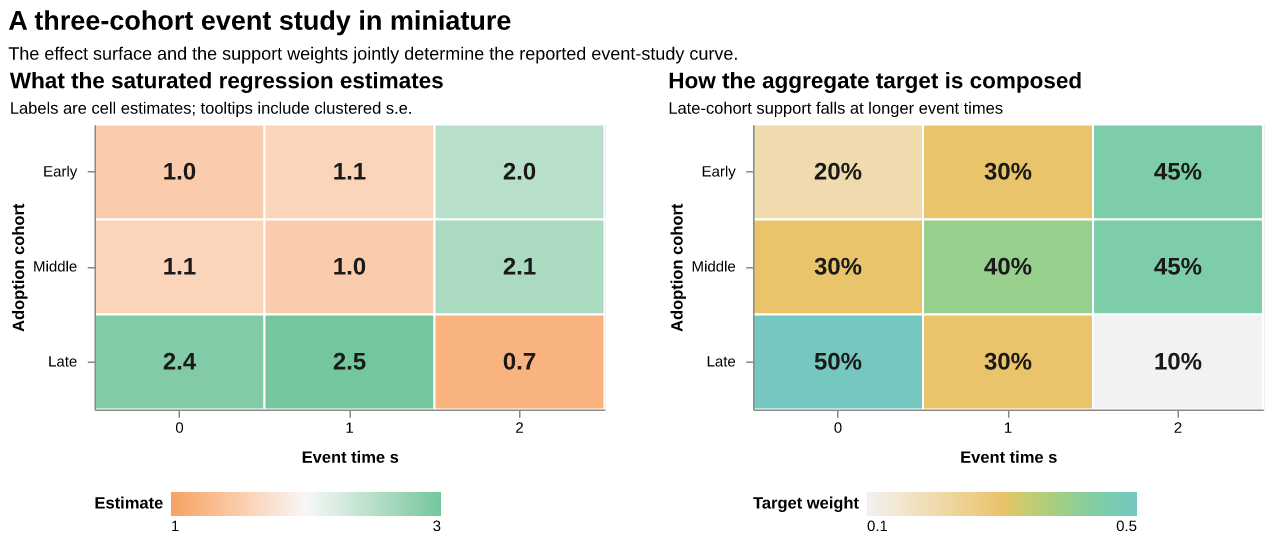

2.4 The estimator in miniature

Consider three adoption cohorts and three post-treatment event times. Suppress one lead period, which remains in its own block throughout the example and is included in each E count below. Figure 1 places the saturated cell estimates beside the weights used to form the aggregate target.

Figure 1: A miniature saturated effect surface and its event-time-specific target weights. Clustered standard errors are 0.35 for the early and middle cohorts and 0.45 for the late cohort. Interactive tooltips report the estimate, standard error, and target weight in every cell.

The left panel has an evident low-dimensional pattern: the early and middle cohorts are similar, their first two effects are nearly flat, and the late cohort follows a different path. The right panel shows why cohort structure can matter for the aggregate curve. The late cohort receives 50 percent of the weight at s=0 and 10 percent at s=2. Applying the displayed weights gives

\hat\tau_{\mathrm{sat}}=(1.73,\ 1.48,\ 1.92).

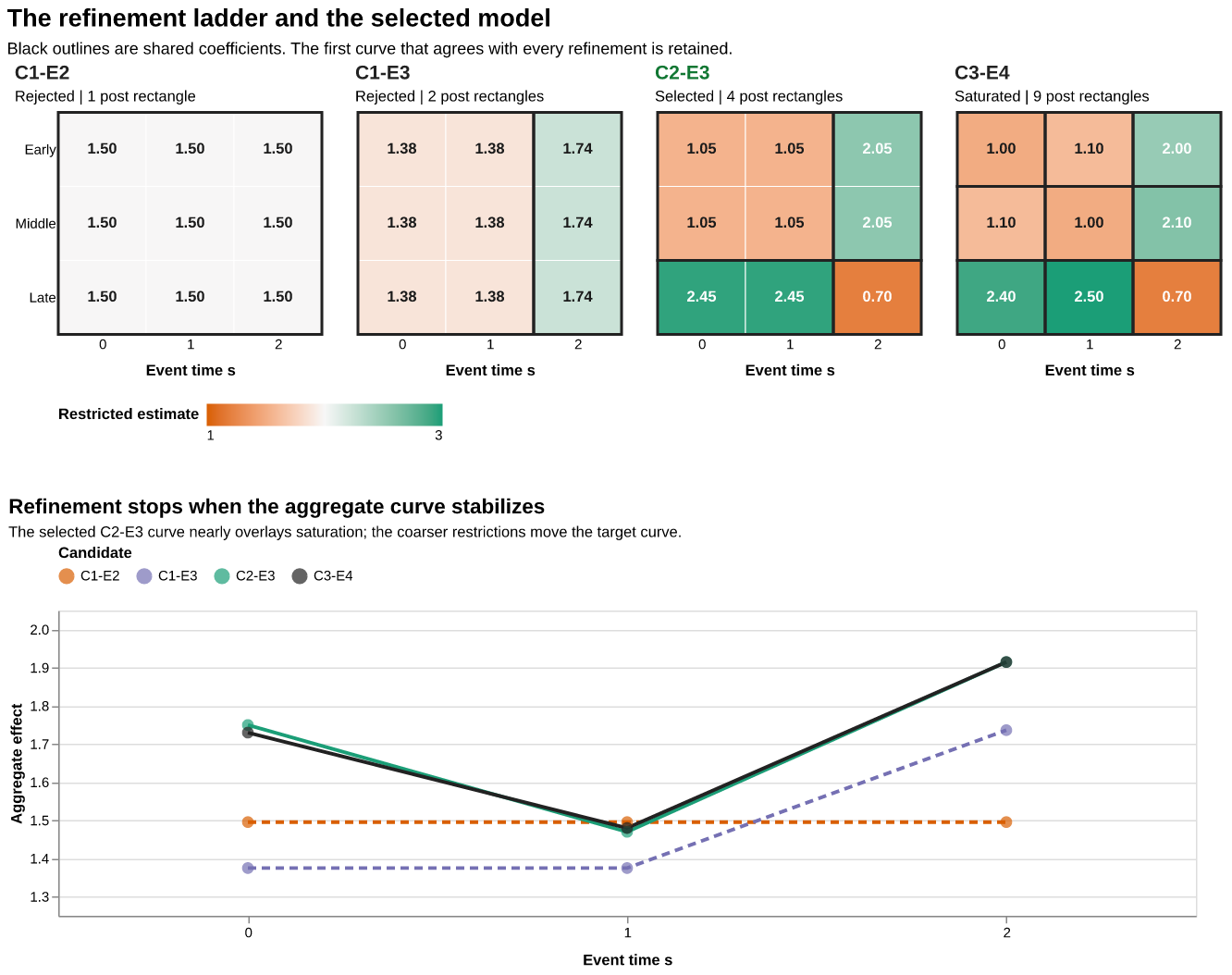

Figure 2 puts four restrictions on a refinement ladder. C1-E2 uses one post-treatment rectangle. C1-E3 splits short and long event times. C2-E3 also splits the late cohort from the early-middle block. C3-E4 is saturated. Every move right splits an existing rectangle, and the lower panel maps each restricted surface back to the same support-weighted curve.

Figure 2: The refinement ladder and its common-target curves. Black outlines delimit shared post-treatment coefficients. Dashed aggregate curves correspond to rejected candidates; green marks the selected C2-E3 model and black marks saturation. Interactive tooltips report cell estimates, restrictions, target weights, aggregate effects, and differences from saturation.

In this illustration, the first two restrictions visibly move the aggregate curve. The C2-E3 curve remains compatible with its saturated refinement, so the rule stops there. Its four post-treatment coefficients are 1.05 and 2.45 for the early-middle and late short-run blocks, and 2.05 and 0.70 for their long-run blocks. Applying the original target weights gives

\hat\tau_{C2-E3}=(1.75,\ 1.47,\ 1.92),

which nearly overlays the saturated aggregate using four post-treatment coefficients in place of nine. The full procedure is visible in the two figures: estimate transparent cohort-event cells, project them onto nested rectangles, map every projection to the same target, and retain the least complex curve that agrees with all refinements. Section 3 develops the projection, comparison covariance, and simultaneous critical value used for that decision.

3. Method: Adaptive Partial Pooling on a Lattice

This section develops the paper’s estimator from beginning to end. Section 2 delivered a saturated vector \hat\theta, its covariance \hat\Sigma, and the common target map L. The task now is to use restrictions on \theta to reduce variance without silently changing L\theta. We first build a nested collection of interpretable restrictions, then project every restricted estimate back to the same target curve, use Lepskii comparisons to decide how much refinement the data require, separate that within-lattice decision from hyperparameter tuning and inference, and finally state the formal limits of the procedure. Together, these consecutive stages form one adaptive estimator.

3.1 Constructing candidate restrictions

The goal of this first stage is to turn the unrestricted cohort-by-event-time surface from Section 2 into an ordered set of plausible lower-dimensional surfaces. This supplies the approximation class for the paper’s bias-variance problem: coarse members pool many cells and can be precise, while fine members retain more heterogeneity and approach the saturated estimator. The nesting structure introduced here is also what makes the later Lepskii comparisons directional and interpretable.

Nested adjacent partitions

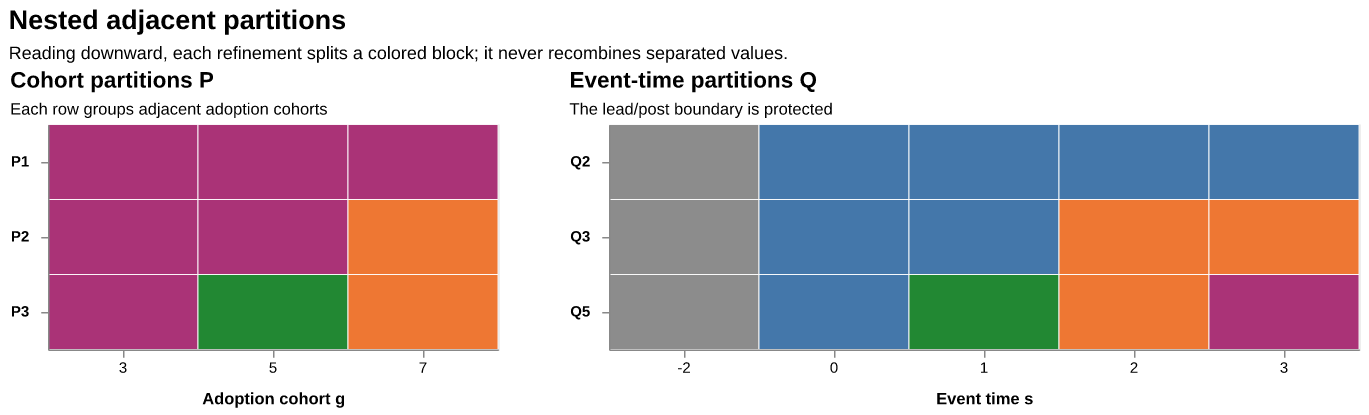

Start with a toy event study containing three adoption cohorts, g\in\{3,5,7\}, and five reported event times, s\in\{-2,0,1,2,3\}. The reference period s=-1 is normalized away. The cohort partitions in this example are

Figure 3: A three-cohort example of nested adjacent partitions. A colored run is one block. Moving downward only splits existing blocks: \mathcal P refines adoption cohorts and \mathcal Q refines event times.

The distinction is concrete. \mathcal P_a says which neighboring adoption cohorts must share coefficients. \mathcal Q_b says which neighboring event times must share coefficients. For example, \mathcal P_2 allows the late cohort to differ from the early and middle cohorts, while \mathcal Q_3 allows the lead, short-run response, and long-run response to differ.

A finer partition splits existing blocks, and every finer block remains inside one coarser block. Thus \mathcal Q_3 refines \mathcal Q_2 because each block of \mathcal Q_3 lies entirely inside a block of \mathcal Q_2. The implementation constructs each path recursively to preserve this containment. Independent equal-width binning at every dimension can violate nesting. The protected break at zero keeps leads and lags in separate blocks.

Crossing partitions into coefficient rectangles

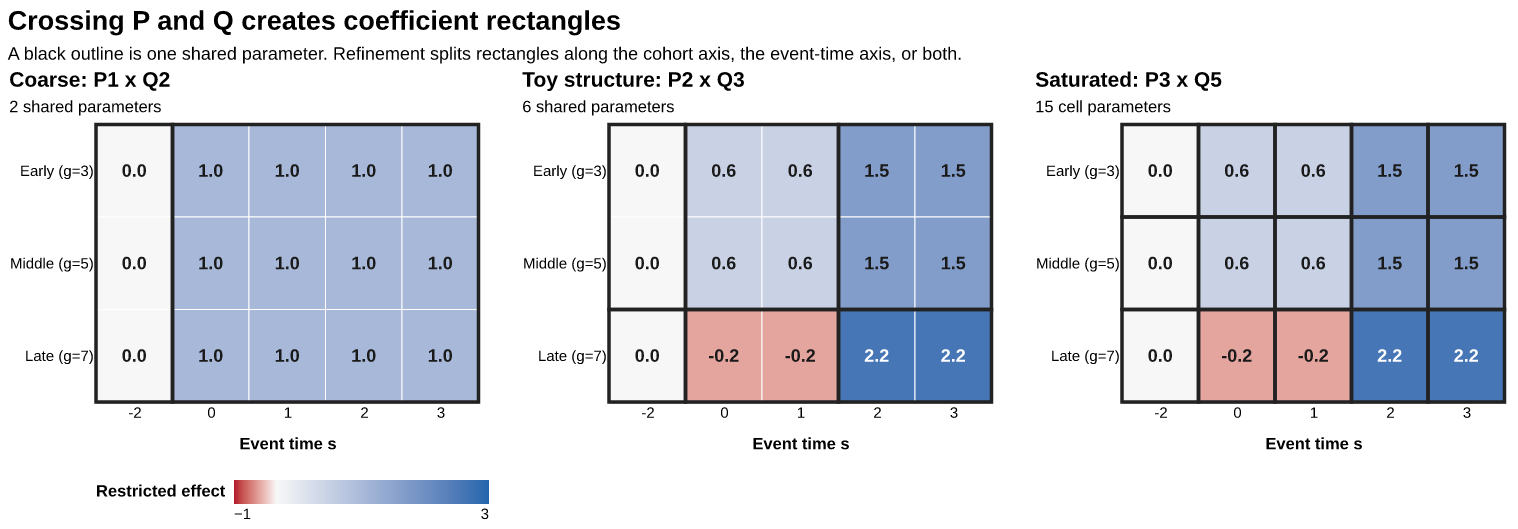

Crossing a cohort partition with an event-time partition turns the two one-dimensional groupings into a restricted treatment-effect surface. In the toy truth below, the early and middle cohorts share a path, the late cohort has a different path, and the post-treatment response has short- and long-run phases. The middle candidate, \mathcal P_2\times\mathcal Q_3, therefore matches the six true coefficient rectangles exactly.

Figure 4: Crossing cohort and event-time partitions. Each black outline is one shared coefficient. The coarse model has two rectangles, the structure-matching model has six, and the saturated model has fifteen. Cell colors and labels show the restricted coefficient value.

The left panel pools all post-treatment cells into one coefficient. The middle panel splits both axes just enough to recover the toy structure. The right panel assigns a separate coefficient to every displayed cohort-event cell. A refinement may split rectangles along the cohort axis, the event-time axis, or both. It weakens restrictions and raises dimension.

Formally, candidate m=(a,b) imposes equality within rectangles of \mathcal P_a\times\mathcal Q_b. Let H_m be the p\times d_m expansion matrix satisfying

\theta=H_m\eta_m

when the restriction is exact. With incomplete support, H_m contains rows for cells in \mathcal I, and parameters correspond to nonempty rectangles.

The partial order is

m\preceq f

\quad\Longleftrightarrow\quad

\mathcal P_f\text{ refines }\mathcal P_m

\text{ and }

\mathcal Q_f\text{ refines }\mathcal Q_m.

This containment relation organizes the candidates as a lattice. We label a candidate with K cohort blocks and R event-time blocks as C_K\text{-}E_R; for example, the middle toy model is C2-E3.

3.2 Mapping every candidate to the common target

The partitions above describe restrictions on the cohort-event surface. The reported object is an aggregate event-study curve. This stage turns each candidate restriction into an estimator of the same \tau=L\theta defined in Section 2. Holding the target fixed ensures that differences between coarse and fine models measure the consequences of pooling under one common estimand.

Minimum-distance projection

It helps to keep the three spaces separate. The vector \eta_m contains one coefficient per nonempty rectangle, \theta contains one coefficient per supported cohort-event cell, and \tau contains one coefficient per reported event time. The matrices below move between those spaces.

Object

Dimension

Role

H_m

p\times d_m

expands d_m rectangle coefficients into p supported cells

P_m

p\times p

replaces a saturated cell surface by its restricted fitted surface

L

q\times p

aggregates supported cells into the fixed q-period target curve

D_m=LP_m

q\times p

maps the saturated estimate directly to candidate m’s target curve

For positive semidefinite metric W, estimate the restricted parameters by

\hat\eta_m

=

(H_m'WH_m)^+H_m'W\hat\theta,

where + denotes a Moore-Penrose inverse. Define

P_m

=

H_m(H_m'WH_m)^+H_m'W.

The first equation chooses the rectangle coefficients whose expanded surface H_m\eta_m is closest to \hat\theta in the geometry defined by W. The second collects that calculation into the projection map P_m. The same base fixed-effects regression supplies every candidate.

Thus \hat\theta_m is useful for inspecting the restricted cohort-time surface, whereas \hat\tau_m is the object compared and ultimately reported. Every \hat\tau_m has the same coordinates and target weights; only the amount of pooling used to estimate it changes.

The production estimator uses feasible GLS, W=\hat\Sigma^+. If model m is correct, this is the efficient minimum-distance estimator under the saturated Gaussian approximation. Under misspecification, it estimates a projection:

A support-weighted projection is also available as a diagnostic. When the same support weights define both the within-event-time projection and L, cohort pooling leaves the aggregate target numerically invariant and offers no meaningful variance gain for that target. GLS weighting converts the equality restrictions into an efficiency gain under the restricted model, with an explicit bias cost away from it.

Joint covariance across candidates

The next selection stage compares candidate curves to one another and therefore requires the covariance of their difference in addition to each curve’s marginal standard errors. All candidates are transformations of the same saturated estimate and are highly correlated; preserving that dependence is one of the main practical benefits of constructing the entire lattice from one base fit.

Adding the two marginal variances would ignore their common saturated fit and substantially overstate comparison noise.

Endpoints and the external comparator

The lattice contains several familiar restrictions:

one cohort block with saturated event time is a common-cohort dynamic curve;

one lead block and one post block with one cohort block is a static pooled restriction, subject to the lead normalization;

saturated cohorts and saturated event times reproduce \hat\theta exactly;

intermediate rectangles represent adoption regimes and dynamic phases.

The common-cohort minimum-distance endpoint differs algebraically from a naive TWFE event study. The simulations estimate naive TWFE in a separate regression and use it as an external comparator outside the lattice.

3.3 Choosing complexity with Lepskii comparisons

The preceding stages produce many estimates of one target curve: coarse candidates have lower sampling variance when their restrictions are adequate, whereas fine candidates are less exposed to pooling bias. This stage decides which precision gains the data support. Its role in the overall paper is to turn the candidate lattice from a menu that a researcher must choose manually into an estimator with a reproducible data-dependent complexity choice.

The selector asks whether relaxing a coarse candidate’s restrictions changes the reported target curve by more than can be explained by the shared sampling noise in \hat\theta. This target-specific comparison allows pooling when latent heterogeneity aggregates away and triggers refinement when heterogeneity materially changes the aggregate target.

Lepskii’s principle answers that question by starting from the precision-favoring end of the lattice. A candidate remains viable only if its curve agrees with all of its finer, less restricted comparators after accounting for uncertainty. The selected model is the least complex viable candidate. This implements a one-sided burden of proof: additional parameters are retained only when a refinement reveals a target-relevant discrepancy.

Pairwise target-curve discrepancies

For a coarse candidate m and a comparable refinement f\succeq m, define

\hat\Delta_{m,f}=\hat\tau_m-\hat\tau_f.

At the population level the corresponding difference is

\Delta_{m,f}

=

L(P_m-P_f)\theta.

If the restriction imposed by m is adequate for the target, both candidates have the same target limit and \Delta_{m,f}=0. If pooling in m distorts the target, at least one refinement can produce a nonzero difference. We compare only nested pairs because f\succeq m has a precise meaning: f relaxes some of the equalities imposed by m and imposes none that conflict with them. Each incomparable candidate receives its own refinement checks. Direct specification comparisons use nested pairs.

Section 3.2 supplied the covariance \hat S_{m,f} of the difference. For each event time, the standardized discrepancy is therefore

The implementation summarizes the entire curve comparison by its largest absolute standardized discrepancy on a prespecified selection set \mathcal S_0:

Large T_{m,f} means that some target coordinate changes too much to attribute to estimation noise; small T_{m,f} supports retaining the coarser candidate. The default \mathcal S_0 contains supported post-treatment event times and excludes the normalized reference period and the weakest tail. This set is part of the scientific decision: it identifies the portion of the curve whose approximation quality governs pooling. The reported curve may include additional event times.

Every finer model contributes information to the comparison. A noisy saturated curve can mask a departure that is visible in a well-chosen intermediate refinement. For example, in the toy surface, a cohort split can reveal the late cohort’s different response before every cohort-event cell is estimated separately. The rule therefore compares each candidate with every finer member of the lattice.

Simultaneous cluster multiplier calibration

The statistic above is searched over event times, over refinements of a given candidate, and ultimately over all candidates considered for selection. A pointwise normal cutoff yields excessive rejection under this search. One cluster multiplier process approximates the joint null distribution of the entire family.

For draw r, generate independent cluster multipliers \xi_c^{(r)} with mean zero and variance one. The perturbation of the saturated vector is

Reusing the draw is important: it preserves the dependence across models and event times induced by their common saturated fit. After standardization by \hat S_{m,f,ss}^{1/2}, let Z^{*(r)} be the maximum absolute perturbation over all comparable (m,f) pairs and all s\in\mathcal S_0. The critical value is the empirical 1-\alpha quantile,

This one threshold accounts jointly for the event-time maximum, every refinement comparison, and the fact that acceptance is checked for multiple candidate models. The bootstrap is used here to calibrate the selection rule; Section 3.4 develops uncertainty statements for the selected treatment-effect curve.

Acceptance and model choice

Candidate m is accepted when

T_{m,f}\leq\hat c_{1-\alpha}

\quad\text{for every }f\succeq m.

Acceptance records statistical agreement with every permitted relaxation at the target-curve level. Surface-level equality remains unassessed. The saturated model is accepted vacuously because its refinement set is empty, which guarantees at least one accepted candidate.

Among accepted candidates, the procedure selects the model with the fewest estimable rectangles. Ties are resolved by fewer cohort blocks, then fewer event-time blocks, then lower estimated target variance. In the toy example, the coarse \mathcal P_1\times\mathcal Q_2 candidate should fail once its pooled curve is compared with refinements that isolate the late cohort and the dynamic phases. If \mathcal P_2\times\mathcal Q_3 then agrees with every finer curve, the rule stops there and avoids the variance cost of fifteen saturated cells.

The full within-lattice procedure can be read as six operations:

Fit the saturated surface once and recover \hat\theta, \hat\Sigma, and cluster influence contributions \hat\psi_c.

Build each candidate map D_m=LP_m and its common-target curve \hat\tau_m=D_m\hat\theta.

For every nested pair, compute \hat\Delta_{m,f} and its shared-fit covariance \hat S_{m,f}.

Use common multiplier draws to obtain one simultaneous critical value.

Retain candidates that agree with every finer comparator.

Report the least complex retained candidate as \hat m and its curve as \hat\tau_{\hat m}.

3.4 Tuning the procedure and reporting uncertainty

Section 3.3 selects a model inside a specified lattice, conditional on choices such as the partition path, projection metric, and selection level. This stage addresses a different problem: how those procedural choices are set and what uncertainty statement is attached to the resulting curve. Keeping the two layers separate is necessary for the paper’s adaptive goal. A simultaneous cutoff accounts for searching within one lattice. Searching across alternative lattices requires independent validation.

selection level \alpha, multiplier distribution, bootstrap draws

fixed for the primary specification; varied in sensitivity analysis

The minimum cell support that defines the target is structural. The minimum support allowed for an intermediate pooled rectangle can be tuned because it changes the candidate grid without changing L\theta.

The implemented basis-family comparison remains within nested piecewise-constant models. The balanced family bisects the largest available block; the front-loaded family uses narrower early post-treatment blocks before allocating resolution to the tail. Splines or other nested smooth bases can enter through the same H_m interface. The reported experiment uses the two piecewise-constant families.

This classification prevents tuning from redefining the scientific question. Structural choices determine the estimand or identifying design and are fixed. Candidate-grid choices determine which bias-variance compromises the selector may consider and can be ranked by independent predictive evidence. Calibration choices govern the conservativeness and numerical accuracy of the search and are prespecified for the primary analysis.

Honest nested cluster splitting

The tuning objective is the risk of the whole adaptive procedure under a hyperparameter configuration h. Each training fold therefore runs the complete procedure from Section 3.3, including its own multiplier calibration and model choice. An independent saturated estimate from the validation fold supplies a restriction-free target benchmark with sampling noise.

Clusters are stratified by adoption cohort, including the never-treated group. An outer split reserves one set of clusters exclusively for inference. The remaining clusters are divided into inner folds. For hyperparameter configuration h and validation fold v, fit the adaptive estimator on the training folds and estimate the saturated target independently in fold v.

For fixed event-time weights a_s, use the noise-corrected loss

Because training and validation clusters are independent, subtracting the validation variance removes this noise floor and leaves the target risk of the training procedure in expectation. Stratification keeps the fold target populations as similar as possible; remaining differences in support are a source of approximation error. The implementation uses inverse-validation-variance weights by default to limit the influence of weakly estimated validation coordinates, and reports equal-weight sensitivity.

Each training fit calibrates its own pathwise multiplier critical value. After inner validation chooses a configuration, that configuration is fit on the full tuning sample to select one lattice model. The resulting model key is then held fixed and estimated on the untouched outer inference sample. Hyperparameters and the model key depend exclusively on the tuning clusters and validation loss.

The outer split adds an independent inference layer to cross-validation. It creates a final sample on which both the hyperparameters and the discrete model choice are predetermined. This clean separation of model construction and uncertainty calculation costs precision.

Three levels of inference

The preceding selection and tuning steps create several possible meanings of a standard error. The software separates precision gains from pooling, protection against model selection, and protection against projection bias into three inferential objects.

Model conditional. Treat the selected model as fixed and use D_{\hat m}\hat\Sigma D_{\hat m}'. These intervals provide model-conditional diagnostics. Unconditional post-selection coverage requires an additional adjustment.

Honest split sample. Use the tuning clusters to select hyperparameters and a model, then estimate on the outer inference sample. Conditional intervals are honest with respect to the tuning and model-selection stage, at a direct efficiency cost. They cover the original target L\theta only when the fixed selected model’s projection bias is negligible. Projection bias persists after sample splitting.

Bootstrap after selection. On the full sample, perturb the saturated estimate with cluster multipliers, rerun selection in every draw, and form percentile intervals from selected curves. This captures discrete model selection conditional on the observed projection matrices. The implementation holds those matrices fixed in each draw, yielding an empirical selection adjustment. Uniformly valid confidence bands require stronger theory.

3.5 What the method guarantees

The previous stages define the complete estimator and its inferential variants. This final part of the method section states the scope of the formal claims. The results explain why candidate curves have tractable joint limits and when the selector removes overly coarse models. The claims cover a fixed finite lattice. Adaptive minimaxity over a growing nonparametric class and uniformly valid full-sample post-selection inference remain open.

Assumptions

The assumptions deliberately attach to the saturated estimator and the finite collection of linear maps built above. They allow the partial-pooling machinery to inherit identification and asymptotic normality without imposing a separate data-generating model for every candidate.

Assumption A (identified saturated limit). Under no anticipation, parallel trends, and overlap, \hat\theta\overset p\to\theta for the supported cells.

Assumption B (joint linearity). The saturated estimator has a cluster-level asymptotic linear representation, \hat\Sigma is consistent, and relevant contrast variances are bounded away from zero after removing deterministic normalizations.

Assumption C (finite nested lattice). The cohort and event-time paths are finite, deterministic, and nested. The target map L and selection set \mathcal S_0 are fixed.

Assumption D (bootstrap validity). The cluster multiplier process consistently approximates the joint Gaussian limit of all standardized (m,f,s) contrasts.

Proposition 1: candidate limits

The first result identifies the estimand of each restricted candidate. It makes the source of any pooling bias explicit and links the projection in Section 3.2 to the common target used by selection.

If \theta\in\operatorname{col}(H_m), then P_m(W)\theta=\theta and \hat\tau_m is consistent for L\theta. Otherwise its probability limit has target bias B_m=L[P_m(W)-I]\theta.

Proposition 2: joint covariance

The second result establishes a joint law for the whole candidate path. It is the formal basis for the difference covariance \hat S_{m,f} and the common multiplier process.

For any finite set of candidates,

\sqrt n

\begin{pmatrix}

\hat\tau_{m_1}-LP_{m_1}\theta\\

\vdots\\

\hat\tau_{m_K}-LP_{m_K}\theta

\end{pmatrix}

\rightsquigarrow

N(0,\Omega),

where block (k,l) of \Omega is D_{m_k}\Sigma D_{m_l}'. This follows by applying a finite collection of linear maps to the saturated influence function. Feasible GLS contributes only higher-order error under consistency and regularity of \hat W.

Proposition 3: exact-structure selection

The third result describes the clean benchmark in which one candidate is the lowest-dimensional adequate representation of the target. It formalizes the selector’s intended behavior in the exact block designs used later as diagnostic finger exercises.

Let m_0 be the lowest-complexity candidate whose target limit equals the target and whose finer candidates share that target limit. Suppose every lower- complexity candidate has at least one comparable refinement and event time for which the standardized population contrast diverges, while Assumptions A-D hold. Then the simultaneous rule rejects every lower-complexity candidate with probability approaching one and accepts m_0 with probability at least 1-\alpha+o(1). With a vanishing selection level satisfying the usual power condition, selection of m_0 is consistent.

Approximate structure is empirically central. When every candidate is an approximation, bias and variance jointly determine the desirable model. The natural oracle is

for reporting loss A. A sharp oracle inequality on the two-dimensional partial order requires additional monotonicity linking target bias and refinement. Without that monotonicity, the theoretical claim stops at exact structure. The numerical study reports regret relative to the best feasible lattice candidate under repeated-sample risk.

4. Implementation

Section 3 defines the estimator as a sequence of partitions, linear projections, joint comparisons, tuning decisions, and uncertainty calculations. This section translates those mathematical objects into the software used in the paper. Its goal is to present the proposed procedure as an operational pyfixest extension for applications and simulations, and to identify the diagnostics exposed to an applied user before the numerical evaluation begins.

LepskiiEventStudy subclasses pyfixest’s DID interface. One saturated pyfixest fit supplies coefficients, CRV1 covariance, residualized scores, and the bread. The implementation verifies numerically that the cluster influence stack reproduces the pyfixest covariance before using it for calibration.

The result object exposes all candidate curves, the acceptance lattice, pairwise statistics, selected partitions, unsupported cells, and conditional or adjusted intervals. LepskiiTuner implements the stratified outer split and inner noise-corrected risk comparison. Tests cover partition nesting, protected breaks, target mappings, unsupported cells, covariance reconstruction, both oracle endpoints, calibration reproducibility, honest cluster separation, and Altair schema validation.

5. Numerical Experiment

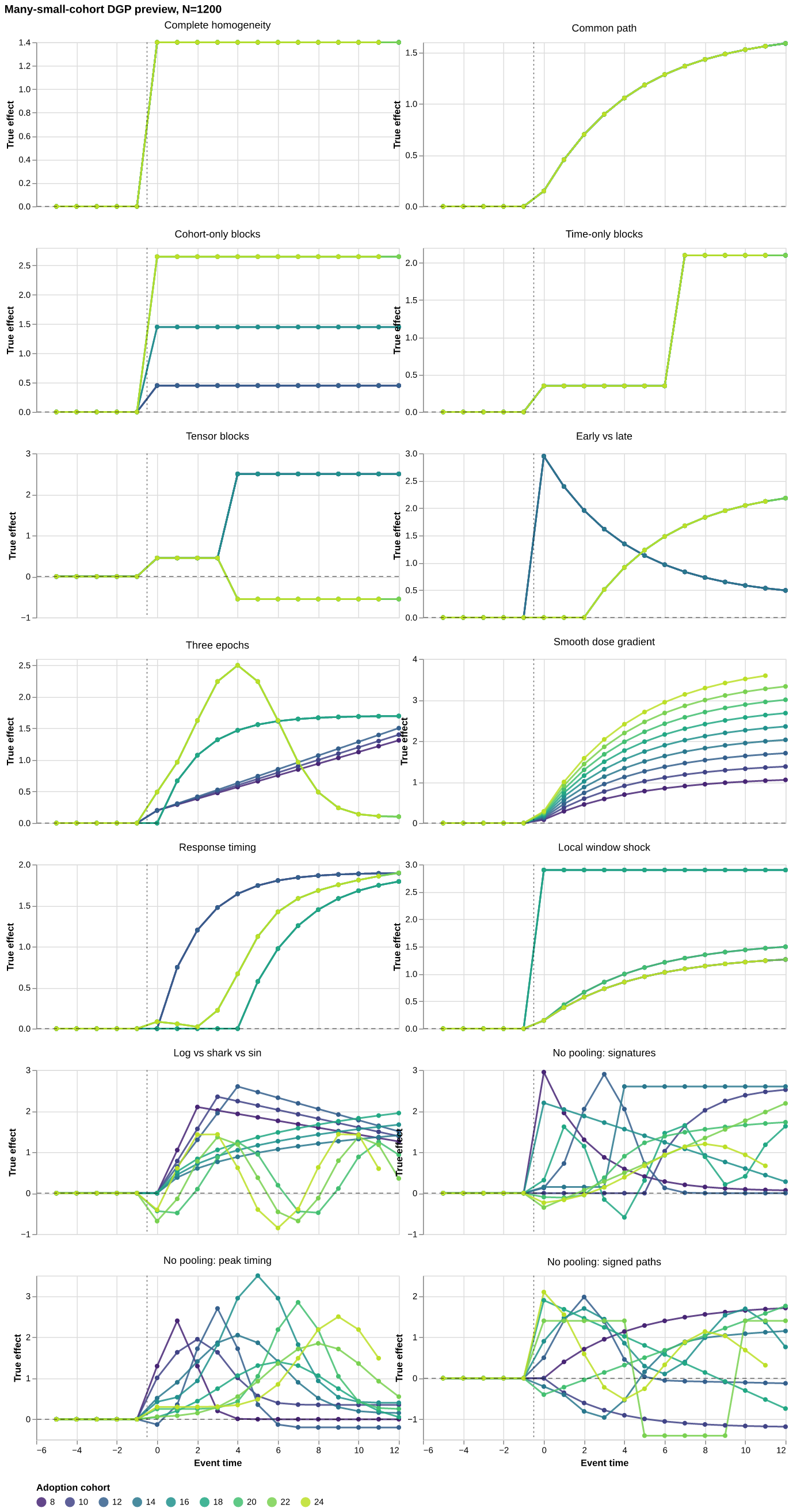

The preceding section establishes how the estimator is computed. This section constructs a controlled many-small-cohort experiment to determine whether those computations solve the paper’s substantive problem: retaining precision when pooling restrictions are useful and moving toward saturation as those restrictions fail. It first defines the treatment-effect surfaces and candidate lattice, then fixes the competing estimators and repeated-sample criteria used in the results.

5.1 Design

The experiment uses T=36 periods and nine treated cohorts adopting in periods 8,10,\ldots,24. Cohort shares are uneven and sum to 0.82; the remaining units are never treated. The main run uses n=1{,}200 units and 50 replications per DGP. Unit, time, and serially correlated idiosyncratic shocks are generated by the repository’s existing panel DGP utility.

The cohort path is

K\in\{1,2,3,5,9\},

and the event-time path is

R\in\{2,3,5,9,17\}.

The 17-bin endpoint separates every reported nonreference event time. Selection uses lags 0 through 11 and 399 Rademacher cluster multiplier draws. The same number of draws is used for bootstrap-after-selection intervals.

The suite includes exact finger exercises and less favorable patterns:

complete homogeneity, with oracle candidate C1-E2;

three cohort-only blocks, aligned with C3-E2;

a common short-versus-long response, aligned with C1-E3;

an early/late long-run interaction, aligned with C2-E5;

smooth gradients, delayed responses, local shocks, and F-test-style log, shark-fin, and sinusoidal curves;

three designs in which every cohort has a distinct path.

Figure 5: True cohort-level treatment-effect paths. The interactive companion retains cohort size, adoption date, latent regime, event time, and true-effect tooltips.

Every method reports a curve on the event-time grid s=-5,\ldots,12, with s=-1 normalized to zero. MSE and bias use the post-treatment selection window s=0,\ldots,11 and the true support-weighted aggregate \tau_s as the reference. The figures and tables use the following six estimator labels.

Naive TWFE. This is a separately estimated pooled event-study regression with unit fixed effects, period fixed effects, and one relative-time coefficient shared by all treated cohorts. The reference period is s=-1 and standard errors cluster by unit. Under cohort heterogeneity, its coefficient can differ from the support-weighted target \tau_s.

Fixed intermediate. This is the C3-E5 lattice candidate in every DGP and replication: three adjacent cohort blocks crossed with five adjacent event-time blocks. Its curve is D_m\hat\theta for model key C3-E5, using the balanced partition path and feasible GLS projection. It measures the performance of a plausible amount of partial pooling fixed before seeing outcomes.

Lepskii selected. This is the primary full-sample adaptive estimator. It searches the balanced lattice with cohort counts K\in\{1,2,3,5,9\} and event-time counts R\in\{2,3,5,9,17\}, calibrates the simultaneous rule with 399 Rademacher cluster multiplier draws, and reports the least complex accepted candidate. Selection and estimation use the same replication sample.

Honest tuned. This procedure reserves half of the unit clusters for final inference. Two-fold noise-corrected validation on the tuning half ranks four prespecified lattice configurations, including balanced and front-loaded paths. The winning configuration runs Lepskii on the full tuning half, and the resulting model key is estimated on the untouched inference half. This computationally intensive comparator is run for ten replications per DGP.

Saturated. This is the C9-E17 lattice endpoint, with one parameter for every supported cohort-event cell. Its reported curve aggregates the saturated cell estimates with the same matrix L used by every lattice candidate. It is the finest fixed candidate and carries the highest sampling variance when the surface admits pooling.

Oracle feasible. For each DGP, we compute the repeated-sample post-treatment MSE of every fixed lattice candidate and choose one model key with the lowest MSE. That same model key is evaluated in every replication of the DGP. The oracle uses the completed Monte Carlo experiment and serves as a fixed-candidate risk benchmark.

The oracle benchmark can lie above an adaptive estimator because Lepskii may choose different candidates in different samples. Naive TWFE can also attain a lower estimated MSE because it lies outside the lattice. Monte Carlo error can produce small negative estimated regret.

Oracle regret is MSE minus the feasible-oracle MSE. We also report squared bias, variance, pointwise coverage, interval length, selection frequencies, and runtime.

Section 5 fixes the DGPs, estimators, and evaluation criteria; this section uses them to assess the adaptive estimator against the paper’s overall objective. The evidence is organized from visual behavior to repeated-sample risk, selected complexity, interval performance, sensitivity, and computation. Reading these objects together evaluates risk, the plausibility of selected structures, and the reliability of uncertainty statements.

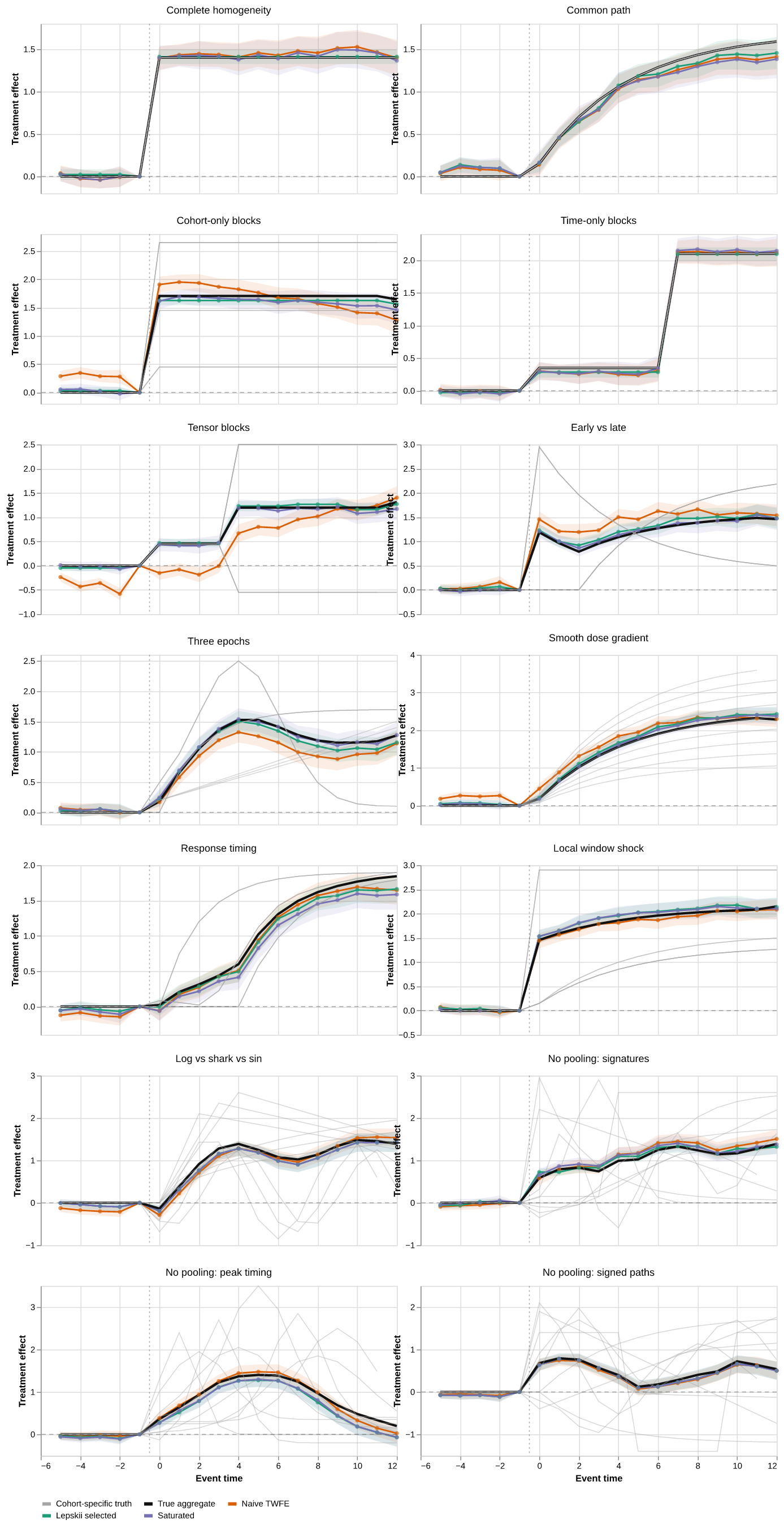

The representative-curve figure displays naive TWFE, full-sample Lepskii, and the saturated aggregate because those three curves expose the pooled, data-adaptive, and fully heterogeneous behaviors in one replication. The risk figure and MSE table compare naive TWFE, the fixed C3-E5 candidate, full-sample Lepskii, honest tuned Lepskii, the saturated C9-E17 endpoint, and the repeated-sample feasible oracle. The selection-frequency figure describes the model keys chosen by full-sample Lepskii. The coverage figure reports model-conditional intervals for naive TWFE, fixed C3-E5, full-sample Lepskii, honest tuned Lepskii, and saturated C9-E17; its interactive tooltips also report selection-adjusted intervals for full-sample Lepskii.

6.1 Representative event-study curves

Figure 6: Representative event-study curves. Light gray lines are cohort-specific truths; black is the support-weighted true aggregate; orange is naive TWFE; green is the Lepskii-selected estimate; and purple is the saturated estimate. Shaded ribbons are pointwise 95% confidence intervals for the three estimators.

The line legend is deliberately separate from the translucent ribbons: light gray denotes latent cohort-specific paths, black the true aggregate target, orange naive TWFE, green the Lepskii-selected curve, and purple the saturated curve. These representative draws illustrate one selected model. The risk and coverage comparisons below use all available replications.

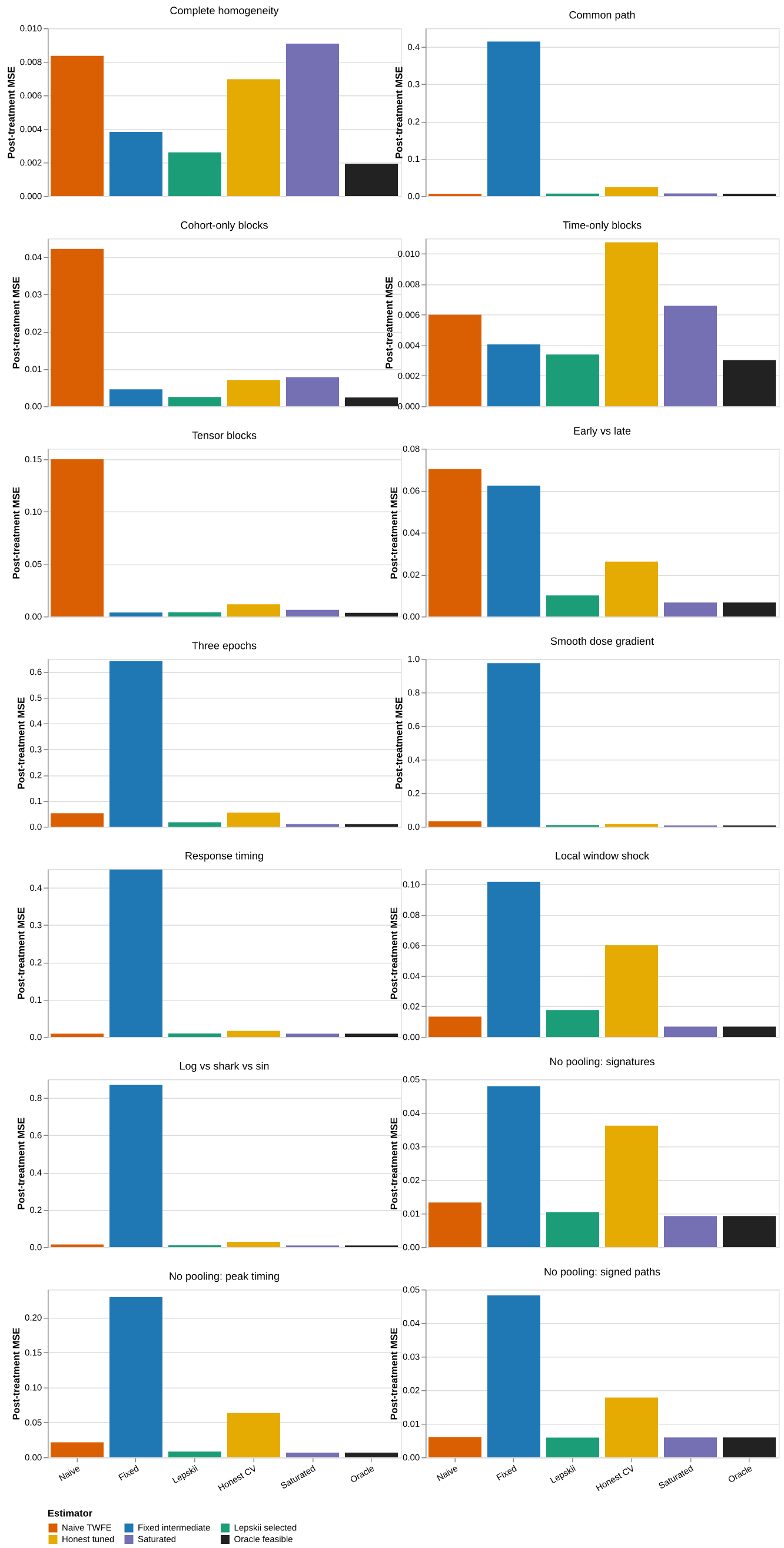

6.2 Risk and oracle regret

Figure 7: Repeated-sample post-treatment MSE by DGP and estimator. Panel scales are independent so that estimator differences remain visible in low-risk designs.

Table 1: Post-treatment MSE relative to the best feasible lattice candidate.

Naive TWFE

Fixed intermediate

Lepskii selected

Honest tuned

Saturated

Oracle feasible

DGP

Cohort-only blocks

17.95

1.94

1.06

3.01

3.33

1.00

Common path

0.95

65.41

1.04

3.72

1.09

1.00

Complete homogeneity

4.33

1.98

1.35

3.61

4.71

1.00

Early vs late

10.59

9.40

1.51

3.94

1.00

1.00

Local window shock

1.97

15.00

2.61

8.87

1.00

1.00

Log vs shark vs sin

1.54

97.01

1.12

3.18

1.00

1.00

No pooling: peak timing

3.24

34.45

1.23

9.55

1.00

1.00

No pooling: signatures

1.44

5.19

1.13

3.91

1.00

1.00

No pooling: signed paths

1.02

8.16

0.99

3.01

1.00

1.00

Response timing

0.99

51.05

1.03

1.85

1.00

1.00

Smooth dose gradient

4.15

123.44

1.17

2.28

1.00

1.00

Tensor blocks

43.12

1.08

1.13

3.37

1.81

1.00

Three epochs

5.20

63.96

1.71

5.43

1.00

1.00

Time-only blocks

1.98

1.34

1.12

3.55

2.18

1.00

The aligned designs provide the cleanest diagnostic. Complete homogeneity should favor the smallest model; cohort-only heterogeneity should refine only the cohort axis; time-only heterogeneity should refine only event time; and the tensor design should refine both. The larger suite then measures how much risk is lost when the true surface is smooth, local, or misaligned with rectangles.

The modal choices in those four diagnostics are, respectively, C1-E2 in 88% of replications, C3-E2 in 86%, C1-E3 in 90%, and C2-E5 in 96%. Their Lepskii MSE ratios relative to the best fixed candidate are 1.35, 1.06, 1.12, and 1.13. Thus the selector reads both axes correctly in the exact block experiments, although selection noise leaves a visible cost even under complete homogeneity.

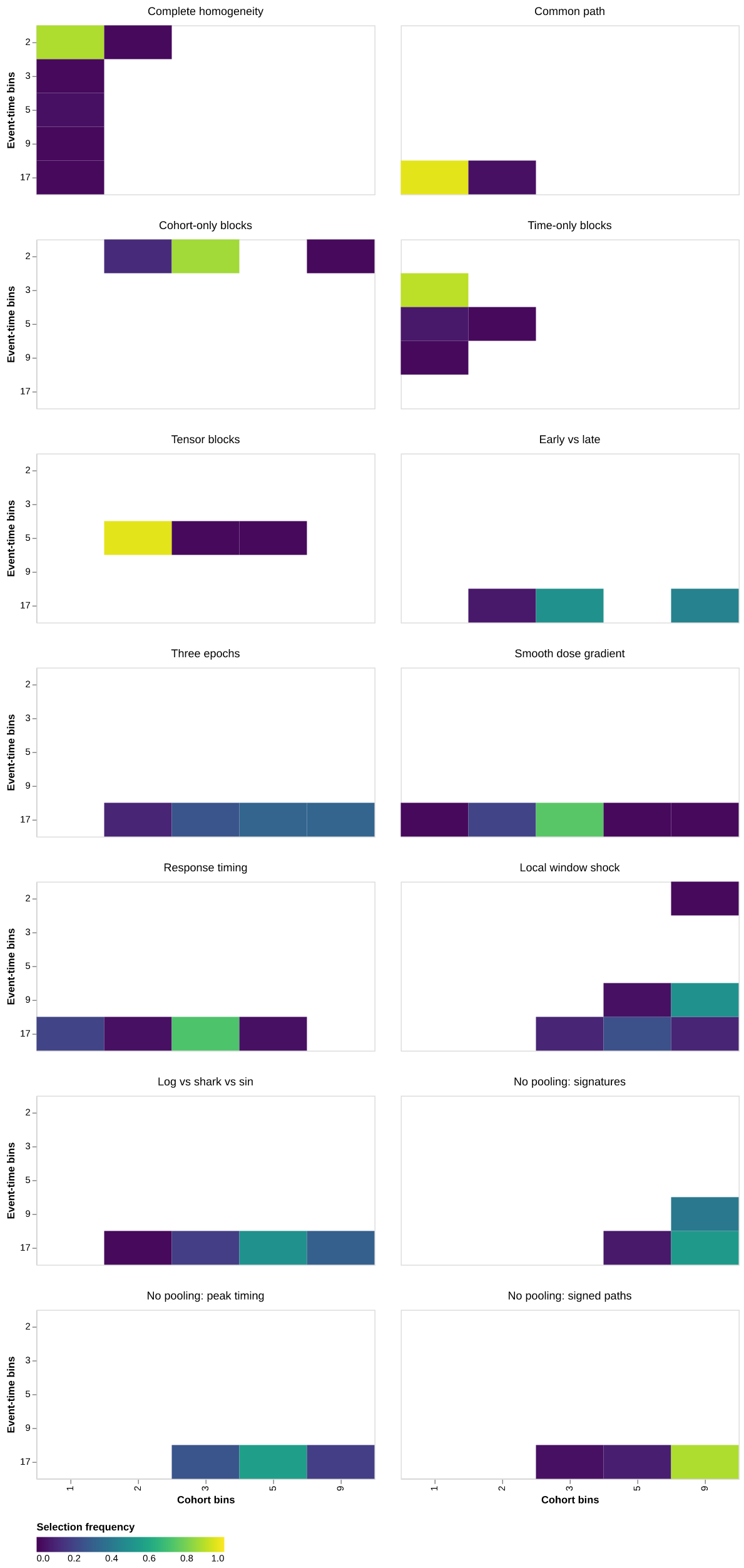

Table 3: Modal selected model and its frequency by DGP.

DGP

Model

Cohort bins

Event-time bins

Frequency

Cohort-only blocks

C3-E2

3

2

0.860

Common path

C1-E17

1

17

0.960

Complete homogeneity

C1-E2

1

2

0.880

Early vs late

C3-E17

3

17

0.500

Local window shock

C9-E9

9

9

0.500

Log vs shark vs sin

C5-E17

5

17

0.500

No pooling: signed paths

C9-E17

9

17

0.880

No pooling: peak timing

C5-E17

5

17

0.560

No pooling: signatures

C9-E17

9

17

0.540

Response timing

C3-E17

3

17

0.720

Smooth dose gradient

C3-E17

3

17

0.740

Tensor blocks

C2-E5

2

5

0.960

Three epochs

C5-E17

5

17

0.320

Time-only blocks

C1-E3

1

3

0.900

Selection is target-specific. In a design with a unique path for every cohort, the oracle may still pool event times if each path has exploitable temporal structure. More subtly, the selector can pool cohorts when their projection bias cancels in the weighted aggregate curve. Such a result supports pooling for the aggregate target and leaves latent cohort homogeneity unresolved. Finer cohort resolution delivered too little target improvement to justify its variance.

The three deliberately non-poolable designs move sharply toward the saturated cohort axis: their modal models are C9-E17, C5-E17, and C9-E17, and their Lepskii MSE ratios are 1.13, 1.23, and 0.99. The modal C5-E17 choice in the middle design retains some cohort pooling, consistent with selection for an aggregate curve. In the signed-path design, the adaptive selector switches among fixed candidates across samples, so its MSE can fall below the best single fixed candidate.

6.4 Coverage and interval length

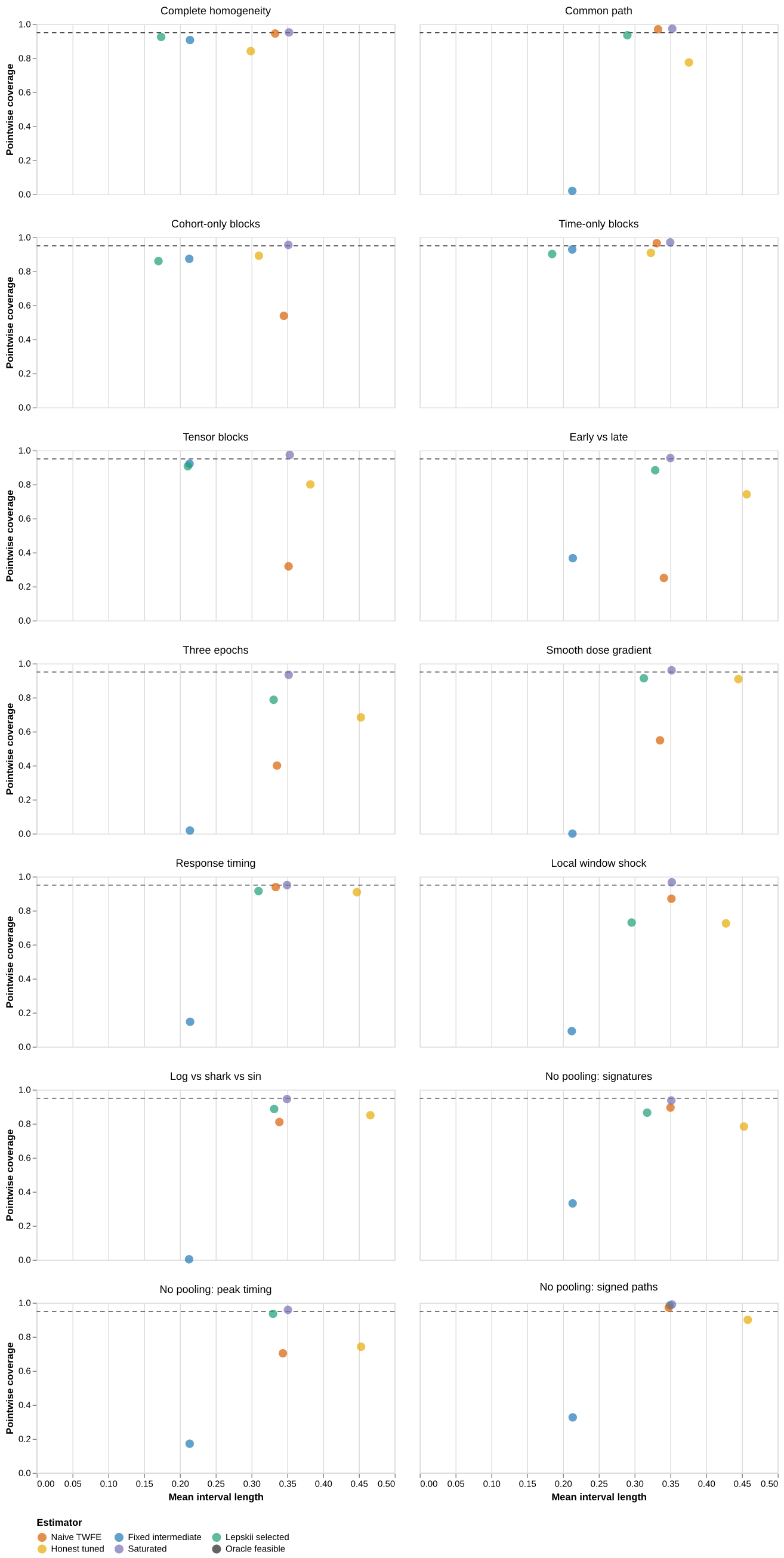

Figure 9: Pointwise conditional coverage against mean interval length. The horizontal rule is 0.95. Adjusted coverage and interval length are available in the interactive tooltips.

Model-conditional intervals are shortest in heavily pooled models. Material projection bias and same-sample selection can produce undercoverage. Bootstrap-after-selection intervals are generally wider. Their reported coverage serves as an empirical selection-adjustment diagnostic; uniform validity remains open.

The localized-shock design is the clearest warning. Lepskii risk is 2.61 times the fixed-candidate oracle and conditional pointwise coverage is 0.73. The bootstrap-after-selection interval raises coverage to 0.965 while increasing mean length from 0.296 to 0.421. Uniform validity remains open. Honest tuning uses only ten replications per DGP and pays heavily for the outer half-sample: its MSE ratios range from 1.85 to 9.55. Its remaining undercoverage is consistent with projection bias that persists after independent selection.

6.5 Sensitivity

The primary selector is rerun for five replications in four representative designs while varying the selection level, lattice density, event-time basis, projection metric, multiplier draws, and multiplier seed. The honest tuner is rerun for three replications in the tensor and non-poolable-signature designs while varying validation-loss weights, the number of inner folds, and the split seed. These deliberately small runs provide stability diagnostics with limited Monte Carlo precision.

Table 5: Sensitivity of honest tuning to loss weights, folds, and split seed.

Axis

Scenario

Designs

Replications

Model agreement

Median MSE / primary

Worst MSE / primary

Fold count

Three inner folds

2

3

0.17

0.91

1.18

Primary

Primary tuning

2

3

1.00

1.00

1.00

Split seed

Alternate split seed

2

3

0.67

1.34

2.59

Validation weights

Equal event-time loss weights

2

3

1.00

1.00

1.00

Model agreement is the share of matched DGP-replication pairs selecting the same lattice model as the primary specification. Risk ratios compare repeated-sample post-treatment MSE within each design before taking the reported median or maximum across designs. The split-seed row is especially important: large movement there signals weak information for fine hyperparameter ranking, even when the outer inference step remains honest.

Multiplier simulation is stable in this diagnostic: both 199 and 799 draws match the primary model in every run, and the alternate multiplier seed agrees in 95% of runs. The substantive approximation choices matter more. The front-loaded basis agrees in 65% of runs, the coarse lattice in 20%, and the equal-weight projection in 80%; the last has a median MSE ratio of 1.35. Within honest tuning, equal event-time loss weights happen to agree in all six matched runs. Three folds agree in 17%, while an alternate split seed agrees in 67% and reaches a worst-design MSE ratio of 2.59. The low replication count yields imprecise rankings and reveals substantial fold and split sensitivity that belongs alongside the tuned result.

The lattice fit performs one fixed-effects regression regardless of the number of candidates. Projection, comparison, and multiplier operations are dense linear algebra on the supported coefficient dimension. Honest tuning is more expensive because independence requires additional saturated fits on cluster subsamples.

7. Limitations

The results show where adaptive pooling succeeds and where local or weakly supported heterogeneity remains difficult. This section relates those empirical failures back to the assumptions and design choices in Section 3 and marks the boundary of the paper’s claims. Its purpose is to distinguish limitations of the current candidate lattice and inferential implementation from failures of the underlying difference-in-differences identification strategy.

First, the method inherits the credibility of the saturated base estimator and its comparison group. A failed parallel-trends assumption invalidates the identified cells before regularization begins.

Second, adjacent rectangles form an interpretable, limited approximation class. A local shock that cuts across the deterministic hierarchy may require more bins than a localized tree or fused-penalty estimator. The candidate grid therefore embodies substantive approximation assumptions.

Third, feasible GLS uses an estimated covariance metric. The reported first- order covariance treats the resulting projection matrices as fixed. This is standard for finite-dimensional feasible minimum distance. Weakly supported cells can make the approximation unstable, making support thresholds and condition diagnostics essential reporting items.

Fourth, the simultaneous Lepskii rule controls a family of model-difference statistics. Unconditional confidence bands for the selected curve require an additional inferential argument. Honest splitting is the clean default when inferential validity is paramount. The full-sample bootstrap adjustment provides a computationally useful empirical correction, and stronger uniform theory remains open.

Finally, a target-curve selector is intentionally insensitive to latent heterogeneity that aggregates away. Researchers interested in cohort-specific effects should select and report a surface-level loss. A coarse aggregate model supports a claim about the aggregate target alone.

8. Conclusion

The limitations above delimit what can be claimed from the current theory and experiment. This final section returns to the paper’s motivating choice between pooled and saturated event studies, summarizes how the proposed estimator changes that choice, and identifies the theoretical and inferential work still needed to complete the broader adaptive-pooling program.

Treatment effects often have low-dimensional structure across adoption cohorts, event time, or both. The proposed estimator uses that structure without changing the reported target: start from a saturated heterogeneity-robust surface, project it onto a nested cohort-time lattice, preserve joint covariance, and select the coarsest model that survives all finer comparisons.

The resulting procedure turns the original joint-test diagnostic into an estimator. It recovers precision when restrictions are supported, returns toward saturation as restrictions fail, and makes the selected structure directly reportable. Its strongest current evidence is finite-grid implementation and simulation performance. A general oracle inequality for approximate models on a two-dimensional partial order and uniformly valid full-sample post-selection bands remain the main theoretical tasks.

Callaway, Brantly, and Pedro H. C. Sant’Anna. 2021. “Difference-in-Differences with Multiple Time Periods.”Journal of Econometrics 225 (2): 200–230.

Chaisemartin, Clément de, and Xavier D’Haultfœuille. 2020. “Two-Way Fixed Effects Estimators with Heterogeneous Treatment Effects.”American Economic Review 110 (9): 2964–96.

Goldenshluger, Alexander, and Oleg Lepski. 2011. “Bandwidth Selection in Kernel Density Estimation: Oracle Inequalities and Adaptive Minimax Optimality.”The Annals of Statistics 39 (3): 1608–32.

Goldsmith-Pinkham, Paul, Peter Hull, and Michal Kolesár. 2024. “Contamination Bias in Linear Regressions.”American Economic Review 114 (12): 4015–51.

Goodman-Bacon, Andrew. 2021. “Difference-in-Differences with Variation in Treatment Timing.”Journal of Econometrics 225 (2): 254–77.

Lal, Apoorva. 2025. “When Can We Get Away with Using the Two-Way Fixed Effects Regression?”arXiv Preprint arXiv:2503.05125.

Lepski, Oleg V. 1990. “A Problem of Adaptive Estimation in Gaussian White Noise.”Theory of Probability and Its Applications 35 (3): 454–66.

Lepski, Oleg V., and Vladimir G. Spokoiny. 1997. “Optimal Pointwise Adaptive Methods in Nonparametric Estimation.”The Annals of Statistics 25 (6): 2512–46.

Sun, Liyang, and Sarah Abraham. 2021. “Estimating Dynamic Treatment Effects in Event Studies with Heterogeneous Treatment Effects.”Journal of Econometrics 225 (2): 175–99.

Wooldridge, Jeffrey M. 2021. “Two-Way Fixed Effects, the Two-Way Mundlak Regression, and Difference-in-Differences Estimators.”Working Paper.

Source Code